BBVA Strengthens its Business with Companies through a Comprehensive Offering in Financing, Advisory, and Innovation

BBVA has elevated the Enterprise segment to one of its strategic priorities to drive growth and value creation. The bank aims to become the strategic partner of choice for companies of all sizes—SMEs, mid-sized companies, large corporations, and institutions—building on its universal banking model, global presence, and capabilities in financing, advisory, technology, and artificial intelligence, as well as the opportunities sustainability offers as a business lever. This roadmap forms part of BBVA’s 2025–2029 Strategic Plan, presented to analysts and investors.

The session held on Tuesday, March 10, focused on the business segment as a distinctive growth driver for the bank, as well as on Mexico, one of BBVA’s core markets.

The event was opened by BBVA CEO Onur Genç, who outlined BBVA’s structural strengths—diversification across high-growth economies, leading franchises, and an innovative culture—which, in his view, are “very difficult to replicate.”

This BBVA Strategic Talks session was led by BBVA CFO Luisa Gómez Bravo, who emphasized transactionality as one of the bank’s key growth levers in its business with companies. During the event, Jaime Sáenz de Tejada, Global Head of Commercial Banking at BBVA, and Javier Rodríguez Soler, Global Head of Sustainability and Corporate and Investment Banking, outlined the growth opportunities in this segment, as well as specific plans to capture them, deliver a radically customer-focused service, and create value.

The Commercial Banking area continues to show strong momentum, with growth of around 10 percent in both loans and deposits in 2025. BBVA currently serves nearly 225,000 business clients¹, with a particular focus on the mid-sized enterprise segment. Within this segment, the bank sees significant potential both in product penetration and cross-selling. As BBVA’s role as the client’s primary bank grows—that is, when the bank becomes the client’s main financial partner—engagement and value creation increase significantly. “When you are a client’s primary bank, you generate twice the revenue, which in turn means more cross-selling, greater income resilience, stronger loyalty, and, of course, higher switching costs,” said Jaime Sáenz de Tejada.

¹The Commercial Banking area covers the business segment starting from revenues above €3–5 million (depending on the geography) up to global clients served by Corporate and Investment Banking.

A transformation focused on the client

Sáenz de Tejada emphasized the importance of understanding how clients operate, the specific challenges of their industries, and anticipating their needs. To support this, BBVA is strengthening its sector-based approach, deepening its understanding of different industries and delivering more specialized advisory services. In his words, “we have adapted our value proposition and are now much better at leveraging sector expertise.”

This approach forms part of a broader transformation designed to strengthen BBVA’s value proposition for companies. The combination of sector specialization, advanced technological capabilities, and a network of professionals with deep client insight allows the bank to deliver increasingly tailored solutions and support companies in their growth, transformation, and international expansion.

Sáenz de Tejada explained how the bank is developing artificial intelligence capabilities integrated into its channels and workflows “to make better decisions, faster decisions, and improve the customer experience.” These tools support clients in their day-to-day operations while equipping relationship managers with advanced analytical capabilities—without compromising the close, specialized relationship model.

Artificial intelligence is also helping simplify processes and reduce friction, creating a faster and more efficient experience. These capabilities automate and prioritize internal workflows while preserving the expert support provided by BBVA’s teams. In lending, data-driven automation accelerates approval processes and enhances consistency in decision-making, while strengthening the quality of analysis and capital discipline. This means companies can access financing more quickly and benefit from a more predictable experience aligned with their needs.

Finally, BBVA is working to integrate the bank’s services—payments, collections, and financing solutions—directly into clients’ systems and operational processes through embedded finance.

A local model with global capabilities

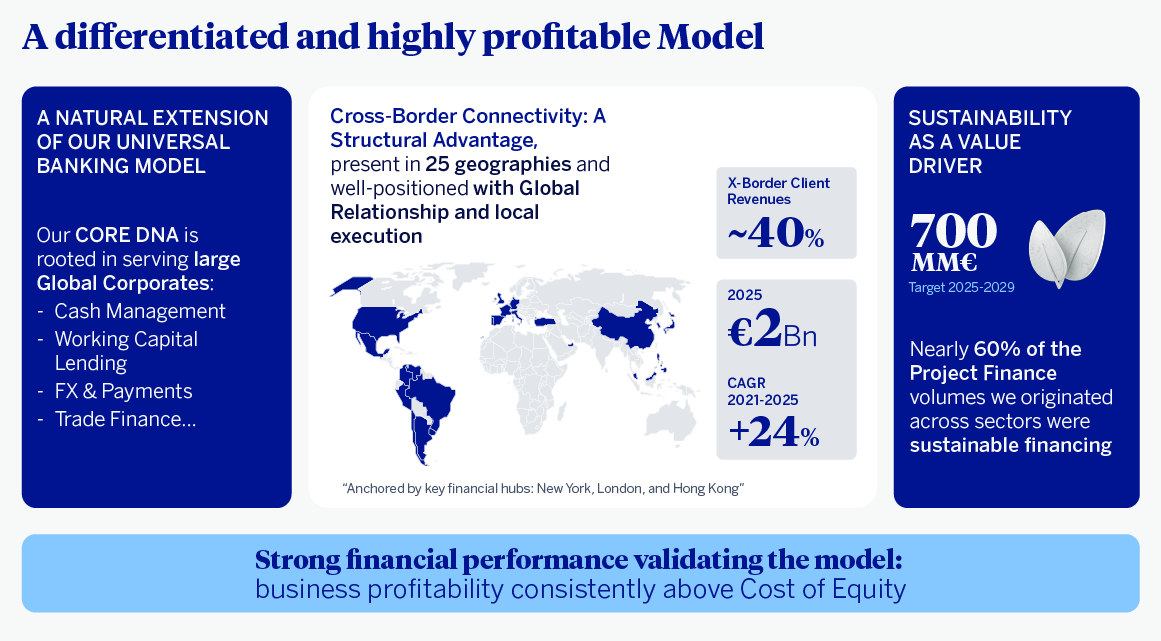

Growth in the business segment is also supported by the strength of BBVA’s universal banking model, which brings together retail banking, commercial banking, and corporate and investment banking (CIB). This model—one priority, three segments, one bank—connects different capabilities across the organization with deep client insight, enabling the bank to deliver comprehensive solutions—from essential transactional services such as payments, collections, and FX management to more sophisticated capabilities, including access to capital markets and structured finance. It also gives BBVA a distinctive ability to operate as a local partner with global reach, delivering a consistent experience regardless of where clients are based or conduct their business.

Javier Rodríguez Soler, Global Head of Sustainability and Corporate and Investment Banking at BBVA, explained that being a universal bank in countries such as Spain, Mexico, Türkiye, Colombia, Argentina, Peru, and Venezuela means serving not only households and small businesses, but also the large corporations that operate in those markets. “It is a natural extension,” he said.

This global presence allows BBVA to support clients across all their financial needs while providing international connectivity. This allows the bank to originate business in one country and execute it in another. “Cross-border business is our main competitive advantage over other banks that do not have this universal banking presence worldwide. We have been growing our cross-border business by 24 percent annually, from approximately 31 percent of gross income in 2021 to over 40 percent last year,” he said. In other words, nearly half of CIB’s activity at BBVA involves clients doing business with the bank beyond their main market.

Profitable and sustainable growth

CIB’s strategy is framed within a disciplined growth model focused on profitability and capital efficiency. “In all our key geographies, our business generates returns that exceed the cost of capital,” said Rodríguez Soler. In his view, international expansion and technological investment are not ends in themselves, but levers for sustainable value creation. In fact, cross-border connectivity drives higher profitability.

Sustainability is another key growth driver in BBVA’s 2025–2029 Strategic Plan. The opportunity remains significant both among mid-sized companies—only 6 percent of which have completed a sustainable financing transaction in the past twelve months—and among large corporations.

In short, in today’s increasingly complex business environment—marked by market volatility, regulatory change, and rapid technological progress—companies are looking for financial institutions that can anticipate their needs and deliver tailored solutions. BBVA meets this challenge by combining its universal banking model with artificial intelligence tools that strengthen the capabilities of its teams and digital channels. This allows the bank to scale its client relationships while maintaining a close and specialized approach.