FOMC: Powell, an Advocate for Optimism

As we expected, the FOMC increased the Fed funds rate to 1.5%-1.75%, confirming that newly appointed Chairman is committed to maintaining continuity with his predecessor. The language in the statement underpinned the committee’s shift from a defensive to potentially offensive mindset, with strong labor market signals, increased business investment and firmer actual inflation readings.

As a result, Wednesday's communication and projections set the stage for a slightly more hawkish policy course than market expectations although consistent with our outlook, which assumes three more rate increases this year. Powell, while shaking off the jitters of his first press conference policy, set out a policy course very similar to his predecessor, side-stepping some of hard-hitting questions on fiscal policy, trade, federal debt issuance and balance sheet normalization, bank stress tests and his appetite for more rate increases this year. Markets whipsawed, but were little changed with respect to equities and bonds.

The changes to the Summary of Economic Projections (SEP) came without surprises and clearly reflected the committee’s optimism for the short-run impact of fiscal policy. In fact, the median projection for GDP was increased to 2.7% in 2018 and 2.4% in 2019, which represents a respective 20bp and 30bp increase from December’s meeting, and 60bp and 40bp since September. Median projections for inflation, however, were only revised slightly upwards in 2019 to 2.1%, confirming the committee’s view that fiscal stimulus would only have a modest impact on inflation. In addition, the committee signaled a slight upward bias to raising rates above long-term neutral projections. This is a clear message that the FOMC stands ready to stop playing catch-up if growth accelerates and labor markets tighten further. Not surprisingly, the inflation forecasts remains well below our outlook, market expectations and consensus, suggesting that they may have to slowly adjust them to the upside in 2018.

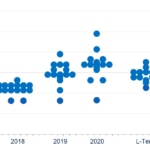

FOMC Dot Plot: Fed Funds Rate, eop, %. - BBVA Research & FRB

At the press conference, Powell noted that the “relationship between slack and inflation is not so tight… reflects flatness of the Phillips Curve”. However, leading up to the meeting, communication from the FOMC members has shifted from discussions on how to confront the risks, anchor inflation expectations and deal with a dearth of fiscal support to how to calibrate monetary policy when fiscal policy is expansionary, inflation is edging up and the output gap is narrowing. When asked in the Q&A session about this shift in approach, Powell said they are “trying to take the middle ground.” This suggests that he is not as concerned about the potential for expansionary fiscal policy to be overly stimulative to the demand-side and thus produce inflationary pressures.

Fed Summary of Economic Projections. - BBVA Research & Bloomberg

Powell also commented that “generally speaking the committee sees the neutral rate of interest as still quite low and is not seeing it as having moved up and is open to the possibility that it will,” which is slightly contradictory when thinking about the tradeoff presented by the expansionary fiscal policy. Powell also mentioned potentially increasing the number of press conferences, although he said his decision would balance transparency with signaling a deviation in the course of monetary policy.

The more hawkish projections and even-handed press conference from Chairman Powell support our baseline projections for three more 25bp increases in 2018. The upward shift in the median path of the Fed Funds rate at the end of 2019 from 2.7% to 2.9% is consistent with our baseline scenario that assumes an interest rate of 3% for the same period.

Led by Nathaniel Karp, the bank’s research team analyzes the U.S. economy and Federal Reserve monetary policy. For its analyses, the economists create models and forecasts for growth, inflation, monetary policy and industries. The Economic Research team also follows a variety of issues that affect the Sunbelt states where BBVA Compass operates. Follow their work on Twitter @BBVAResearchUSA.