Earnings: BBVA Posts Nearly €3 Billion Profit in the First Quarter (up 11%) and Announces a New Tranche of Share Buybacks

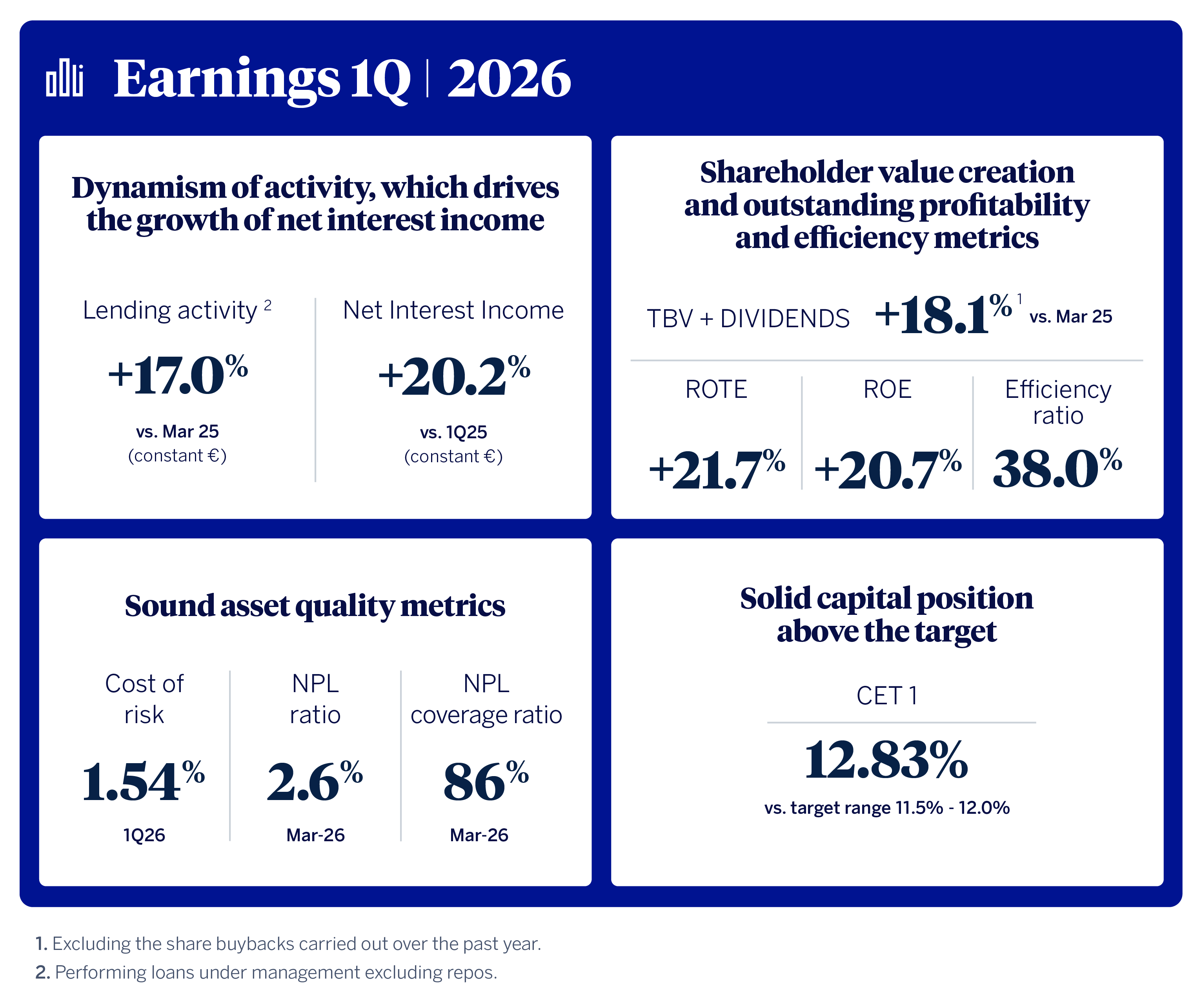

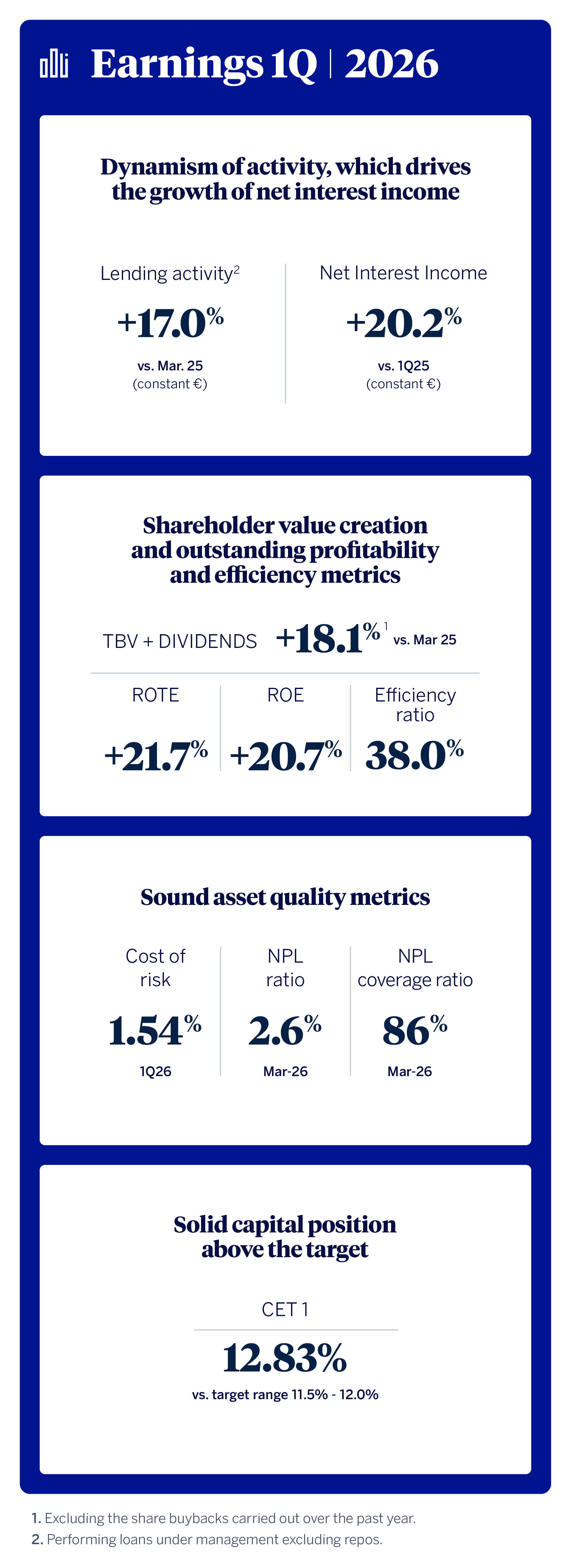

BBVA reported a profit of €2.99 billion in the first quarter of 2026, a 10.8% increase yoy (up 14.1% at constant exchange rates), supported by momentum in the banking business: customer loans grew 17% (at constant exchange rates), boosting net interest income by more than 20% yoy. This growth was accompanied by high levels of profitability and value creation for shareholders: ROTE stood at 21.7% and tangible book value per share plus dividends rose 18.1% yoy¹. All this with a solid capital position, with the CET1 ratio reaching 12.83% at the end of March. On May 6, BBVA will begin the final tranche of the extraordinary share buyback program, with a maximum amount of €1.46 billion.

Press Kit

- Quarterly Report 1Q26 (PDF)

- Results Presentation Analysts 1Q26 (PDF)

- Download video for TV (Tranxfer BBVA)

- Statement from Onur Genç in English (Audio) (Tranxfer BBVA)

- Download video for webs (YouTube)

- Statement on BBVA 1Q26 earnings from Onur Genç (Text) (Tranxfer BBVA)

- BBVA CEO Onur Genç (JPG)

- Ciudad BBVA (JPG)

{kind=link}

{kind=link}

“Our results this quarter indicate that we are making progress in the execution of our Strategic Plan and are on track to achieve the goals set for 2028. All this in a complex geopolitical context, demonstrating the strength of our business model and diversification,” said Onur Genç, CEO of BBVA.

Momentum in the banking business in the first quarter of 2026 led to 17% growth in lending (in constant euros). The strong performance of two of the group’s main markets, Mexico and Spain, was particularly notable, with yoy growth of 8.4% and 6.3%, respectively³. Also noteworthy was the excellent performance of Rest of Business area, which saw a 54.5% increase in activity.

Except where otherwise stated, the evolution of each of the main headings and changes in the income statement described below refer to constant exchange rates. In other words, they do not take currency fluctuations into account.

Performance was very positive across the main lines of the income statement (net interest income, fees and commissions, gross income, operating income and net attributable profit).

Starting with net interest income, it reached €7.54 billion (up 20.2% yoy), mainly driven by Türkiye, South America and Mexico. In addition, the ratio of net interest income over average total assets also continued to show very favorable momentum in recent quarters (3.35% in the first quarter of 2026 compared to 3.29% a year earlier), underscoring the bank’s ability to generate robust interest income, due to higher growth in more profitable segments. Net fees and commissions rose 15.5% yoy to €2.26 billion. Fees linked to payment methods, asset management and insurance stood out, as did the greater contribution of the wholesale banking business (CIB). Core revenues totaled €9.79 billion, an increase of 19.1%.

Net trading income contributed €915 million (up 1.1% yoy), supported by momentum in the Global Markets unit. By business areas, performance was positive in Mexico, Rest of Business, Spain and Türkiye.

The other operating income and expenses line item posted better results in the first quarter of 2026 than in the same period the previous year, thanks to favorable performance in insurance.

Thus, gross income amounted to €10.65 billion, an increase of 18.3% yoy. This solid growth in income, which outpaced expenses growth (up 17.5% yoy), allowed the bank to maintain positive jaws. The efficiency ratio stood at 38%, improving 24 basis points from the previous year.

Consequently, operating income grew 18.7% yoy, reaching €6.60 billion.

Impairment on financial assets amounted to €1.82 billion, broadly in line with the previous quarter, although 35% higher than the first quarter of 2025. This increase occurred against a backdrop of credit growth, especially in more profitable segments. As a result, the loan portfolio coverage ratio increased to 86%, while the non-performing loan ratio improved to 2.6%. The cost of risk ended the first quarter at 1.54%, in line with the previous quarter.

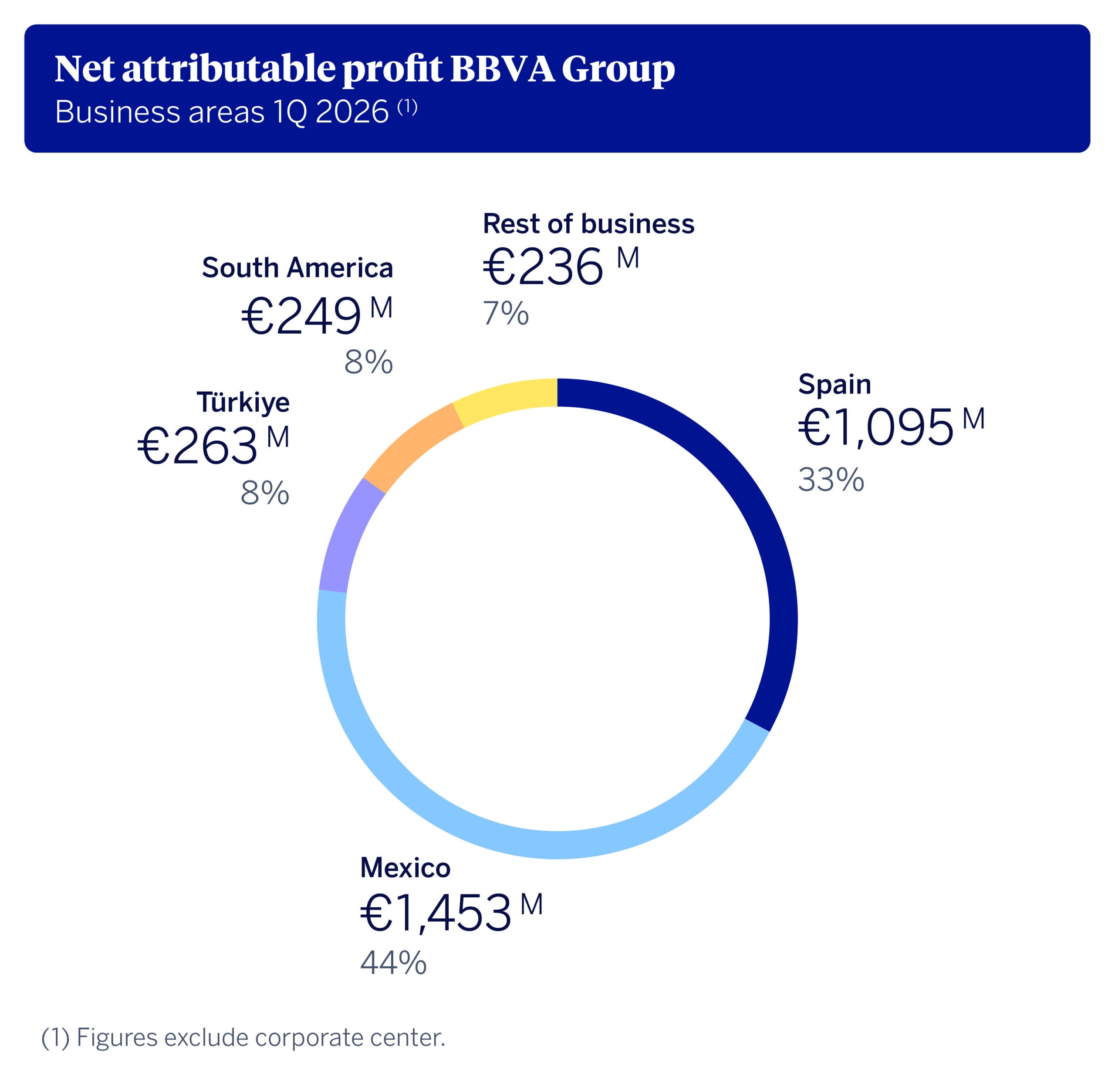

BBVA reported net attributable profit of €2.99 billion in the first quarter of 2026, 14.1% higher than one year earlier (up 10.8% in current euros). Earnings per share grew at an even faster pace (up 12.5% in current euros) thanks to share buybacks carried out over the past 12 months.

The strong quarterly results were reflected in the profitability metrics, with ROE reaching 20.7% and ROTE 21.7%. The group also continued to create value for its shareholders. Tangible book value per share plus dividends rose 18.1%, excluding the share buybacks carried out over the past year.

The final tranche of the extraordinary share buyback program will begin on May 6, with a maximum amount of €1.46 billion. BBVA will have repurchased nearly €4 billion in shares since last December.

BBVA continued to generate capital organically in the first quarter of 2026. The CET1 ratio reached 12.83% (up 13 basis points from year-end 2025), exceeding its target range of 11.5% to 12%. The bank therefore maintains its commitment to distribute any excess capital above the upper end of this range⁴.

Advancing the Strategic Plan and transformation

The first quarter 2026 results represent a new boost in the execution of the Strategic Plan and the financial targets for the 2025-2028 period:

This quarter, BBVA has made decisive progress in its transformation strategy, particularly in artificial intelligence (AI). The bank has eight initiatives that embed AI across the value chain, from Blue, its personal digital advisor for each customer, and AI tools for bankers, to assistants for risk, operations and software development.

Beyond these initiatives, BBVA is moving toward a truly AI-driven model by renewing its operating system and industrializing the creation, governance and deployment of AI agents at scale. Although still at an early stage, promising results are already emerging. Looking ahead, BBVA’s key differentiating factor will be its ability to scale AI across the Group, as it did with its digital transformation.

Business areas

In Spain, lending grew by 6.3% yoy, driven by the business and consumer segments³. Momentum in the banking business was reflected in the recurring revenue (net interest income rose 3.6% and net fees and commissions increased 3.5%, in line with expectations). Net trading income (NTI) also stood out, with 20% growth, fueled by the strong performance of the insurance business and portfolio sales throughout the quarter. This positive trend in revenue resulted in net attributable profit of €1.10 billion, 8.1% more than the same period in 2025. The non-performing loan ratio fell to a historically low level (2.9%) and the coverage rate increased to 69%, while the cumulative cost of risk stood at 0.34% (in line with the end of 2025).

In Mexico, lending increased by 8.4% yoy, or 10.4% excluding the appreciation of the Mexican peso against the dollar over the past twelve months, with balanced contributions from the business and retail segments³. The strong performance of all revenue streams and the excellent efficiency ratio (30.8%) stood out on the income statement. Net attributable profit reached €1.45 billion (up 4.5% yoy). Risk indicators remained solid: the non-performing loan ratio stood at 2.6%, the coverage ratio was 129% and the cumulative cost of risk reached 3.45%.

In Türkiye, growth in loans in Turkish lira was particularly notable (+45.3% yoy). On the income statement, net attributable profit rose 66.1% at current exchange rates to €263 million, driven in large part by recurring revenue. In terms of asset quality, the non-performing loan ratio stood at 4.1%, the coverage ratio was 74% and the cumulative cost of risk was 2.53%, in line with the previous quarter.

In South America, lending grew 15% yoy, driven by loans to businesses and consumer lending. This business area posted a net attributable profit of €249 million, 16.3% more than the first quarter of 2025 (in current euros). The performance of Colombia was particularly notable, with profit increasing significantly to €78 million thanks to strong recurring revenues and lower loan-loss provisions. Peru and Argentina reported net attributable profits of €81 and €27 million, respectively, underpinned by the positive trend in recurring revenue in both cases. In terms of risk indicators, the non-performing loan ratio stood at 4.2%, the coverage ratio stood at 90% and the cumulative cost of risk was 2.76%.

Finally, Rest of Business area saw a significant increase in lending (up 54.5% yoy), driven by the CIB business in the U.S., Europe and Asia. The area reported net attributable profit of €236 million (up 36% yoy), supported by robust gross income. In terms of credit risk, the non-performing loan ratio came in at 0.14%, the coverage ratio was 197% and the cost of risk stood at 0.3%.

About BBVA

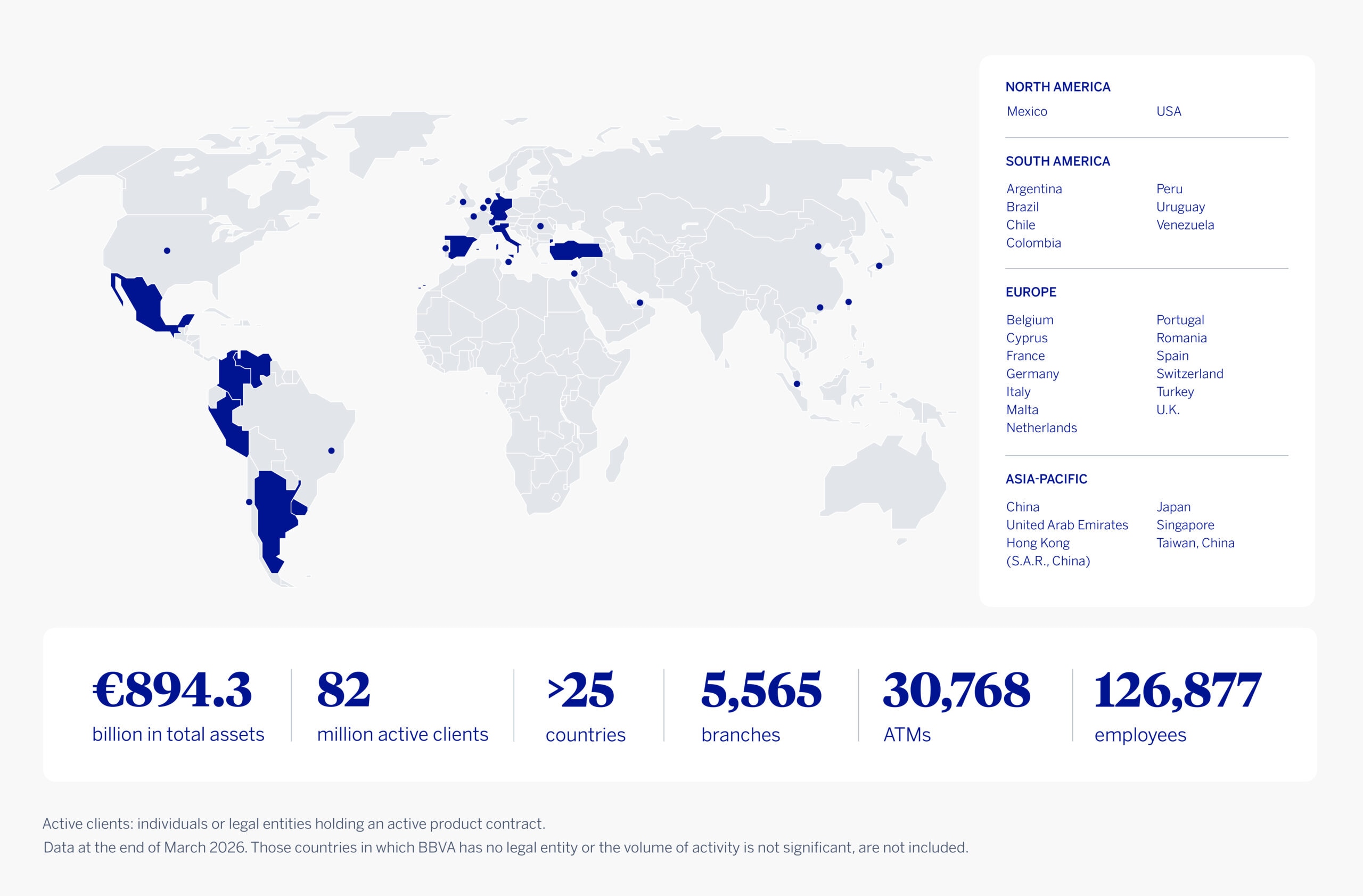

BBVA is a global financial group with a customer-centric vision, characterized by its pioneering strategy in digitization, innovation and sustainability. BBVA holds a leading position in Spain, is the largest financial institution in Mexico, and has leading franchises in South America and Türkiye. In Europe, BBVA has a steadily growing presence, driven by its specialized offices serving business customers and its focus on digital banks, currently operating in Italy and Germany. In addition, BBVA provides specialized services to large corporations through its offices in the United States and Asia. This strong geographic diversification, together with high levels of customer acquisition through digital channels, positions us to strengthen our leadership and address the challenges of the future. BBVA contributes with its activity to the progress and welfare of all its stakeholders: shareholders, clients, employees, providers and society in general. In this regard, BBVA supports families, entrepreneurs and companies in their plans, and helps them to take advantage of the opportunities provided by innovation and technology. Likewise, BBVA offers its customers a unique value proposition, leveraged on technology and data, helping them improve their financial health with personalized information on financial decision-making.