BBVA earns €1.14 billion in 3Q20, 79 percent more than the previous quarter

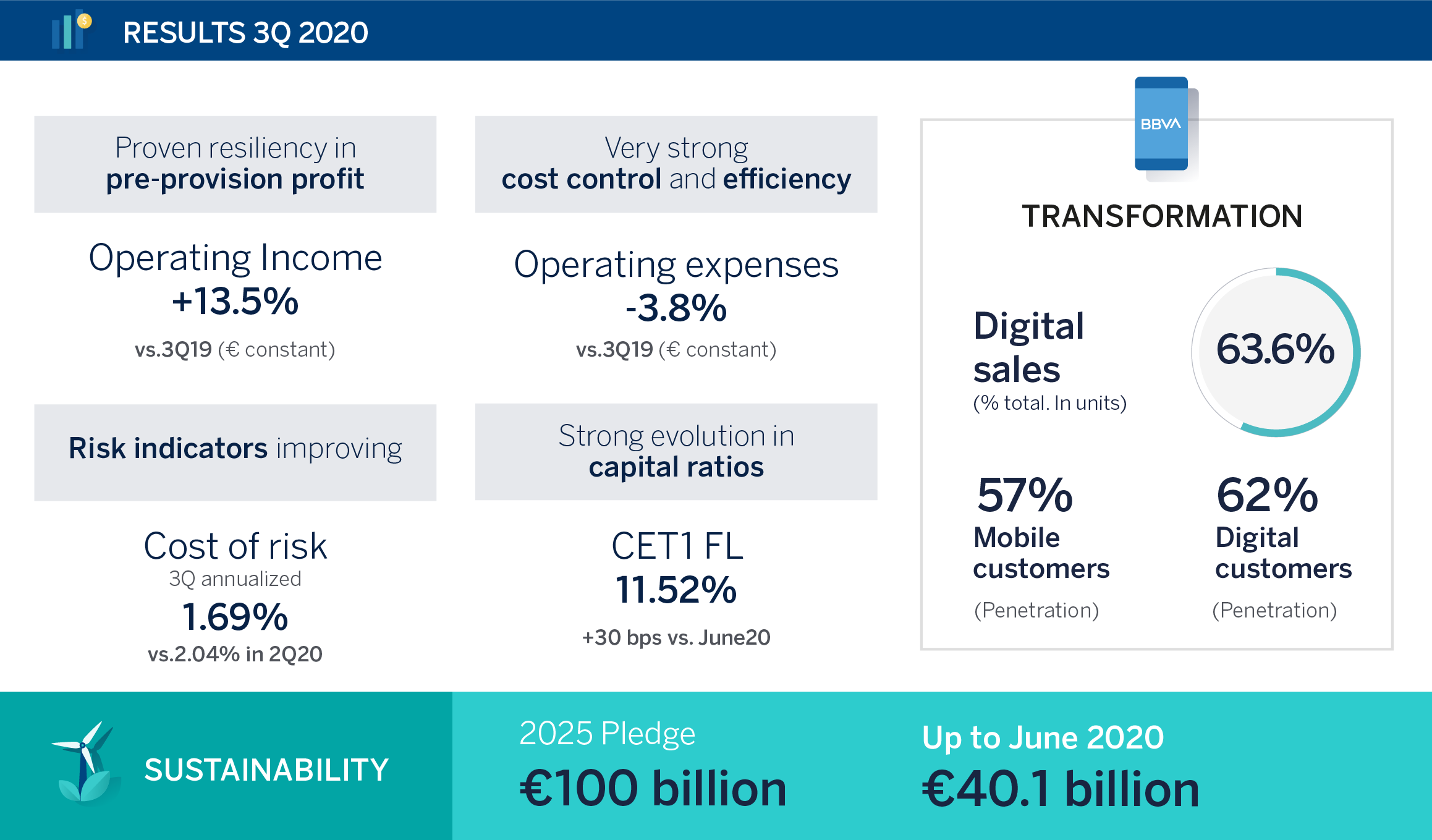

BBVA earned €1.14 billion in the third quarter of 2020. It is the best quarterly result of the year and far exceeds the figure for 2Q20 (+79.5 percent in current euros, +83.4 percent at constant rates). Compared to the same period a year earlier, the 3Q20 result is 6.8 percent lower (+4.1 percent at constant rates). The strength of recurring revenues and cost containment efforts drove quarterly operating income to grow 13.5 percent yoy at constant exchange rates. In a challenging context marked by the pandemic, BBVA has shown a solid capacity to generate capital, with risk indicators having a positive performance. BBVA’s quarterly results also beat market expectations by 48 percent, as analysts’ consensus expected a result of €773 million.

Press kit Results 3Q20

- Statements from Onur Genç (YouTube)

- Quarterly Report 3Q20 (PDF)

- Onur Genç: “This result shows a more normalized level, in line with previous years”

- 3Q20 Results Presentation Analysts (PDF)

- 3Q20 Results Presentation Press (PDF)

- Statements from Onur Genç - Radio

- Statements from Onur Genç - TV

- Statement on BBVA 3Q20 earnings from BBVA CEO (Text)

- 'La Vela', main building in the 'Ciudad BBVA' (JPG)

- Onur Genç, BBVA’s CEO (JPG)

{kind=link}

{kind=link}

“Net attributable profit grew significantly in the third quarter compared to previous quarters. This positive performance has been the result of our resilient recurrent income, coupled with our focus on cost control and a better evolution of impairments, given the significant provisioning effort of the first half of the year,” said BBVA CEO Onur Genç.

The bank’s results have improved throughout 2020, mostly on the back of lower impairments on financial assets and provisions. Additionally, over the past three months, there’s been a recovery of activity in retail banking in all markets, which is reflected in third quarter results.

In order to offer a better comparison for each line of the account, variations hereafter are shown at constant exchange rates.

In the income statement, net interest income grew 5.5 percent in 3Q20 yoy (+4.9 percent vs. 2Q20) to €4.11 billion. In the first nine months of the year, this item reached €12.76 billion, 4.7 percent more than in the same period of 2019. Net fees and commissions fell 0.8 percent yoy in 3Q20 (+12.9 vs. the April-June period), to €1.14 billion. Between January and September, this heading stood at €3.44 billion (-1.3 percent yoy).

Net trading income (NTI) performed particularly well in 3Q20, standing at €372 million (+13.3 percent yoy).

Gross income stood at €5.66 billion in the third quarter, growing 5 percent yoy (+6.2 percent vs. the previous quarter). Between January and September, gross income grew 7.4 percent, to €17.71 billion.

In the third quarter, the bank maintained its focus on containing operating expenses, which fell 3.8 percent yoy, to €2.57 billion. Expenses dropped 2.4 percent to €8.08 billion yoy through September, which is very significant when taking into account that average inflation in BBVA’s footprint stood at 4.4 percent over the past 12 months. Containment in operating expenses and the positive evolution of recurring revenues in the quarter allowed for operating jaws to remain in positive territory. The efficiency ratio at the end of September stood at 45.6 percent (compared to an average of 63.6 percent of its EU comparable peers), which represents a decline of 438 basis points vs. 2019 figures.

Operating income continued to show resilience and grew at double-digit in 3Q20, to €3.09 billion, up 13.5 percent yoy. Through September, the figure stood at €9.63 billion, up 17.3 percent from the same period of the previous year.

BBVA earned €1.14 billion between July and September (+4.1 percent vs. 3Q19). This result is 83.4 percent higher vs. 2Q20. In the first nine months of the year, net attributable profit reached €2.07 billion (-36.6 percent yoy) excluding the goodwill impairment in the U.S. in the first quarter (€-2.08 billion). Including this impact, the net attributable profit stood at €-15 million.

Following front-loaded provisions in the first quarter, with a cost of risk of 2.57 percent, this metric continued to improve: going from 1.51 percent in the second quarter to 0.97 percent in the third, in line with expectations. The accumulated cost of risk since January improved from 2.04 percent in 1H20 to 1.69 percent at the end of September. NPL and coverage ratios were stable in the quarter, standing at 3.8 percent and 85 percent, respectively.

BBVA’s phased-in CET1 stood at 11.99 percent at the end of September, while the fully-loaded CET1 ratio stood at 11.52 percent, which represents a capital generation of 30 basis points compared to June (11.22 percent). BBVA Group’s goal is to keep a buffer exceeding its new CET1 ratio requirement (currently at 8.59 percent) within a target range of 225 to 275 basis points. The current level is above this target (293 bps), a milestone achieved by the bank earlier than expected.

The BBVA Group keeps a solid position in terms of liquidity, with a Liquidity Coverage ratio (LCR) of 159 percent and a Net Stable Funding ratio (NSFR) of 127 percent, both above regulatory requirements (100 percent).

In a challenging context, the tangible book value per share remained virtually stable, and closed the quarter at €5.84 per share.

As for the balance sheet and activity, loans and advances to customers (gross) closed the quarter at €379.02 billion, 4.2 percent above the 2019 year-end figure. Compared to December 2019, the corporate portfolio is still showing a slight increase, although significantly below that of 1H20, as companies stockpiled massive amounts of liquidity through the different government-backed support programs across the Group’s footprint. Customer deposits increased 8.7 percent through September to €495.17 billion, shored up by the strong performance of demand deposits.

Growth in digital customers

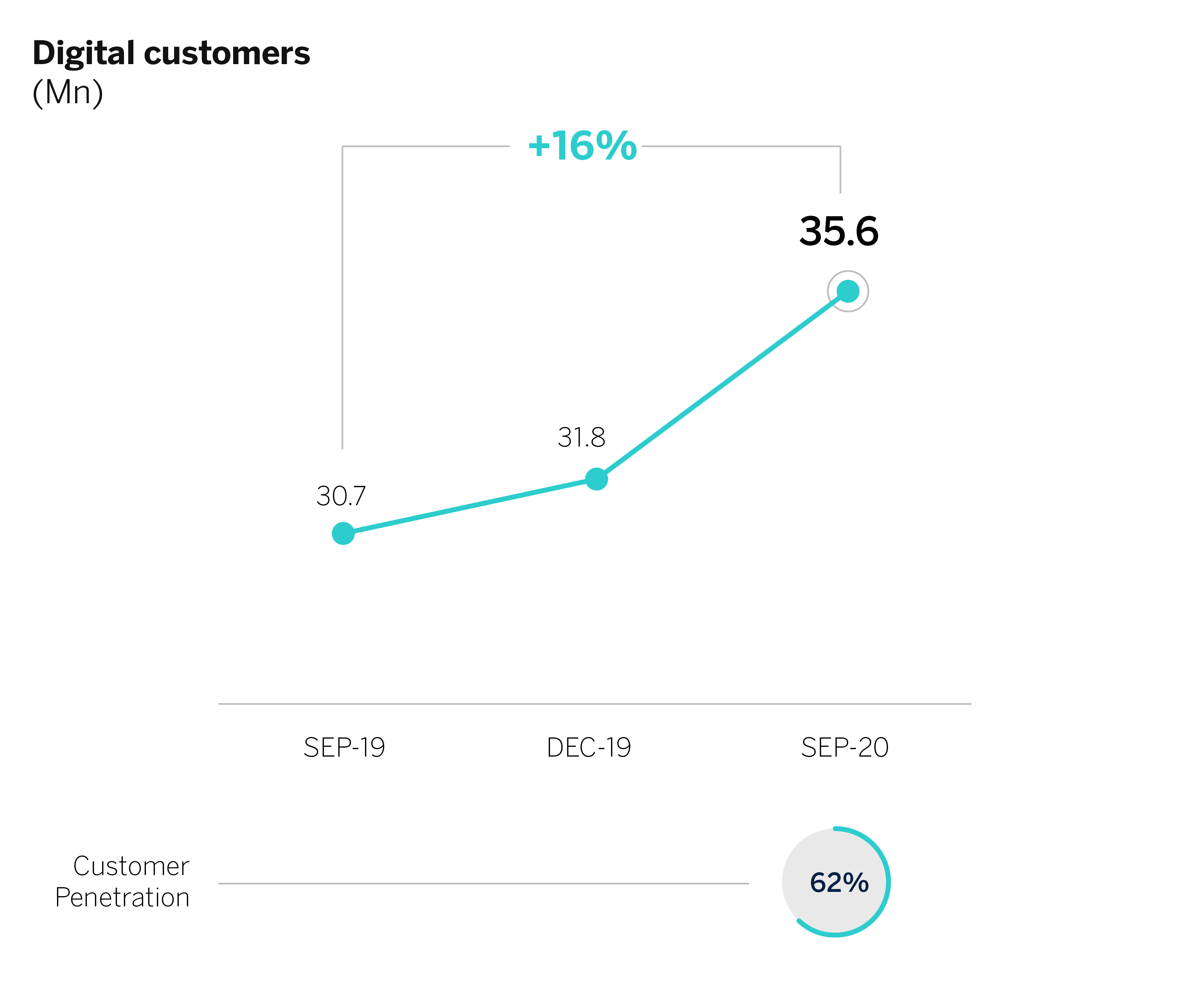

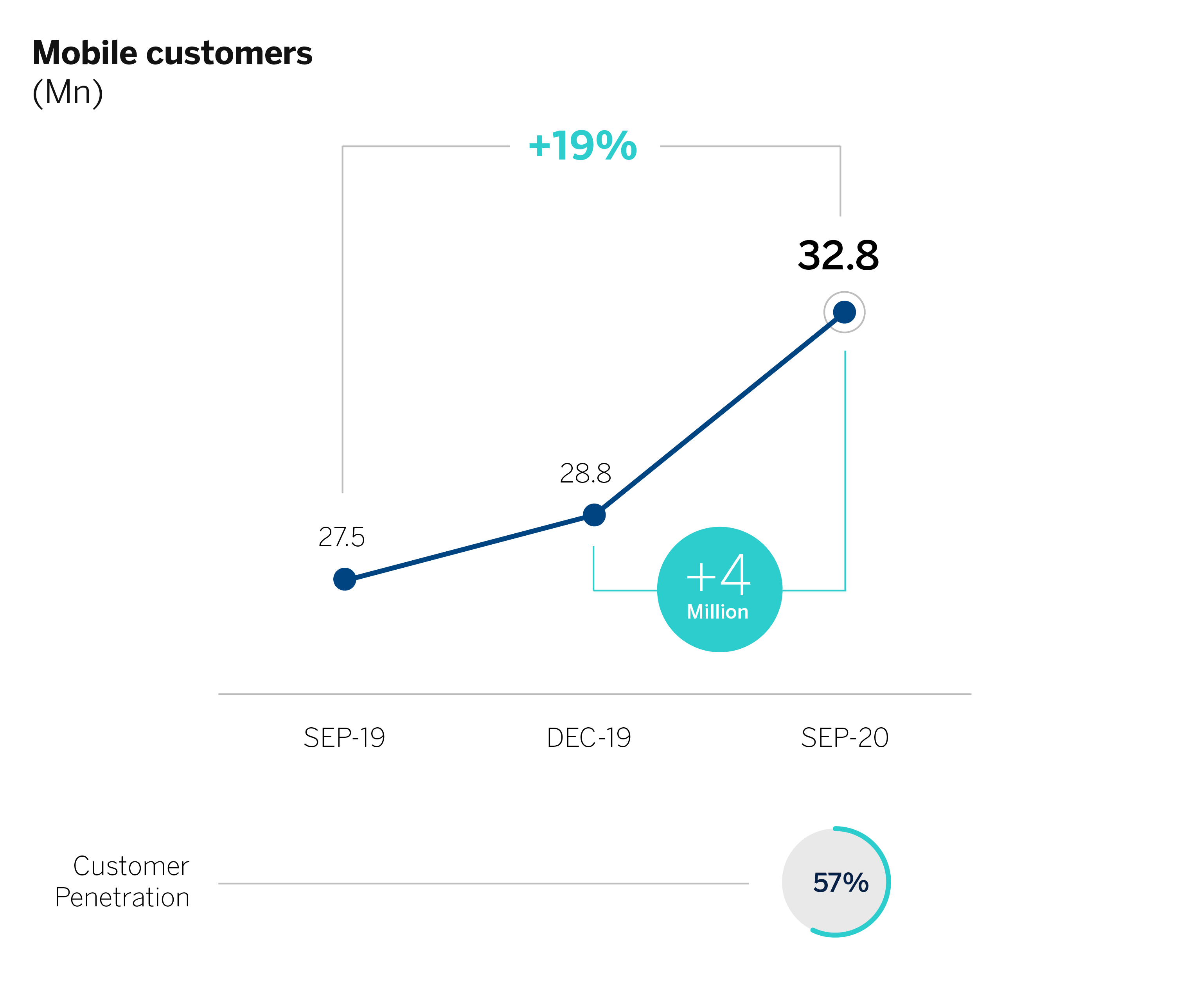

The health crisis caused by COVID-19 is accelerating digitization. Between January and September alone, the bank added more than four million new mobile customers (+14 percent), to 32.8 million (57 percent of the total). Digital customers grew 12 percent compared to Dec. 2019, to 35.6 million (62 percent of the total). Interactions with BBVA’s mobile apps multiplied by five compared to the previous year. BBVA’s positioning in mobile banking stands out. For example, BBVA’s mobile app is the most used in Spain, with 22.2 percent of banking app users, according to consulting firm SmartMe Analytics. In Mexico, the bank has a leading market share in ecommerce, with 39 percent, thanks to its unique digital capacities and payment solutions.

Business Areas

Below you may find the key aspects of activity and the P&L statement for the different business areas.

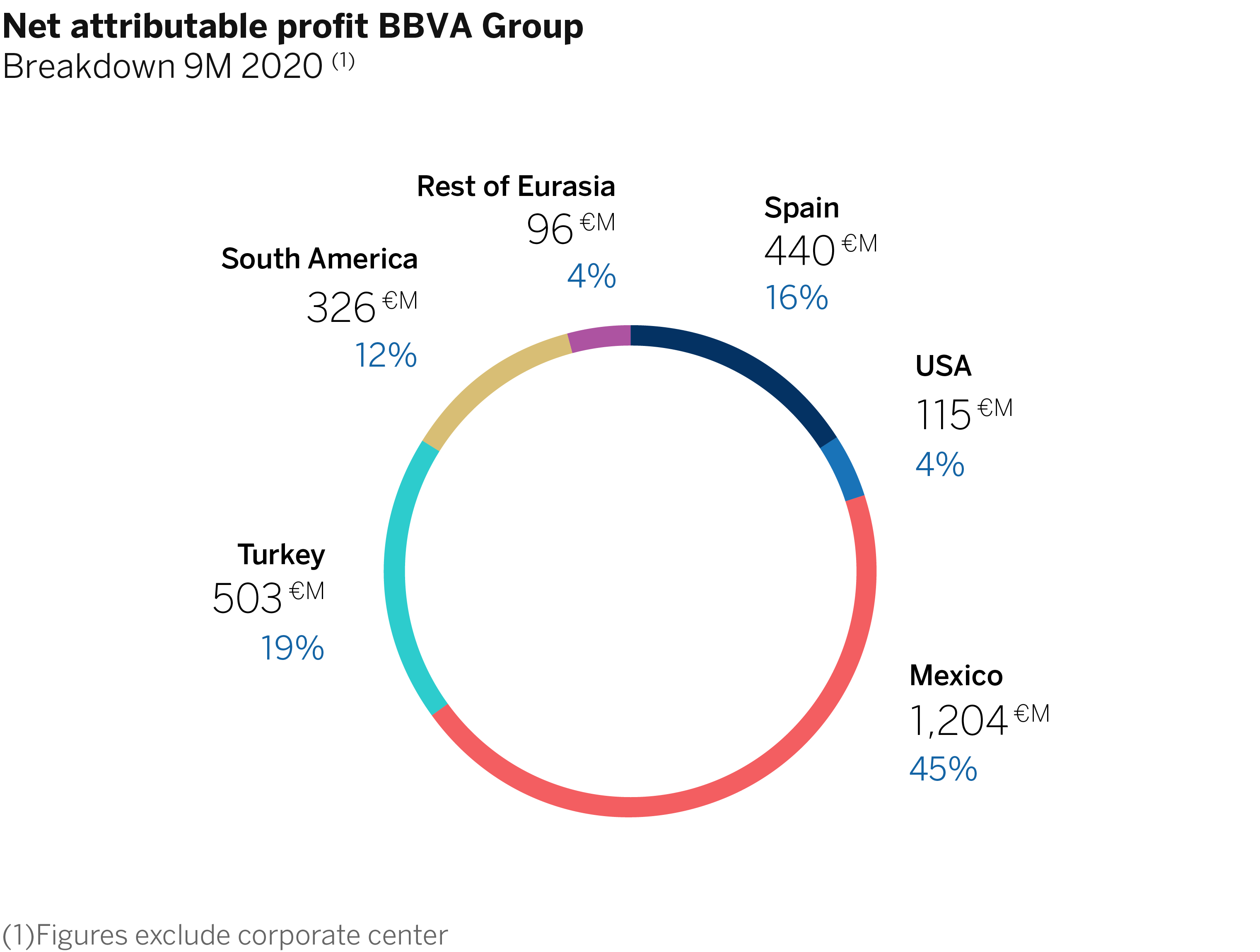

In Spain, corporate banking and SMEs, both driven by government-backed loan schemes, helped lending activity to grow 0.8 percent yoy. Customer funds grew 4.6 percent yoy, bolstered by the growth in demand deposits (+11.7 percent). As for the P&L account, gross income grew 3.2 percent yoy through September thanks to a good performance of net fees and commissions and NTI. Operating income rose 16.6 percent yoy in the first nine months of the year, also as a result of cost containment efforts: operating expenses fell 6.7 percent, the biggest drop over the past five years. The area earned €440 million between January and September, 58.7 percent less than the same period a year earlier, due to impairments on financial assets and provisions, mostly in 1H20. Lower provisions in 3Q20, however, drove net attributable profit to grow 6.5 percent yoy – 54.2 percent vs. 2Q20 – to €352 million. As for risk indicators, NPL and coverage ratios stood at 4.32 percent and 67.6 percent, respectively. After a strong increase in 1Q20, the cumulative cost of risk continued to improve, standing at 0.80 percent in September.

In the United States, lending activity increased 6.3 percent yoy, also thanks to the corporate banking and SME segments, helped by the U.S. Government’s support program. Customer deposits grew 17 percent compared to the previous year, driven by demand deposits. In the P&L account, it is worth noting a strong growth yoy in recurring revenues (NII and net fees and commissions) and a drop in expenses yoy. Between January and September, gross income declined 2.4 percent. Operating expenses fell 2.5 percent, resulting in operating income of €960 million (-2.4 percent). The area’s net attributable profit through September stood at €115 million, down 75.8 percent yoy, mainly as a result of impairments on financial assets recorded in 1Q20. With regards to risk indicators, the NPL ratio stood at 1.93 percent, coverage ratio was 94.5 percent, and the cost of risk continued to improve, to 1.69 percent.

In Mexico, corporate banking, mortgages and the public sector helped lending activity to increase 5.7 percent yoy. Customer resources grew 14.3 percent yoy on the back of demand deposits and, to a lesser extent, off-balance sheet funds. The P&L account improved significantly in 3Q20 compared to the previous quarter thanks to the growth in recurring revenues, containment in operating costs and lower provisions. From January through September, gross income grew 0.4 percent, to €5.23 billion. Operating income reached €3.49 billion (+0.1 percent). The net attributable profit through September was €1.2 billion, down 30.5 percent due to the impact of impairments on financial assets mostly in 1H20. The area earned €567 million, up 88.1 percent compared to 2Q20. The cost of risk continued to improve, to 4.27 percent through September. The NPL ratio stood at 2.29 percent, with coverage ratio standing at 170.2 percent.

In Turkey, lending activity increased 34.3 percent yoy, driven mainly by growth in Turkish lira loans, which was supported by commercial and consumer loans. Customer deposits continued to be the main source of funding for the balance sheet. Customer funds grew 36.3 percent yoy. Turkey’s results show the strength of its operating income, which grew 49.6 percent ytd on the back of good performance of activity and customer spreads. The net attributable profit for the first nine months stood at €503 million, up 58.6 percent from the same period a year earlier. In 3Q20, the attributable profit stood at €252 million, up 84.8 percent, above the previous quarter. The cost of risk continued to improve, to 2 percent as of Sept. 30. The NPL ratio stood at 7.11 percent and the coverage ratio was 81.9 percent.

In South America, lending increased 13.1 percent yoy as of the end of September. The wholesale portfolio performed particularly well, as a result of greater drawdowns of credit facilities by companies in response to the situation created by the COVID-19 health crisis. Customer funds grew 19.4 percent yoy, mostly driven by demand deposits. Net attributable profit for South America stood at €326 million through September, down 30.1 percent, due mainly to higher impairments on financial assets in 1H20. Following front-loaded provisions earlier in the year, net attributable profit in 3Q20 stood at €182 million, up 111.8 percent vs. 2Q20. The cumulative cost of risk for the year reached 2.49 percent, with NPL ratio standing at 4.3 percent and coverage ratio at 110 percent.

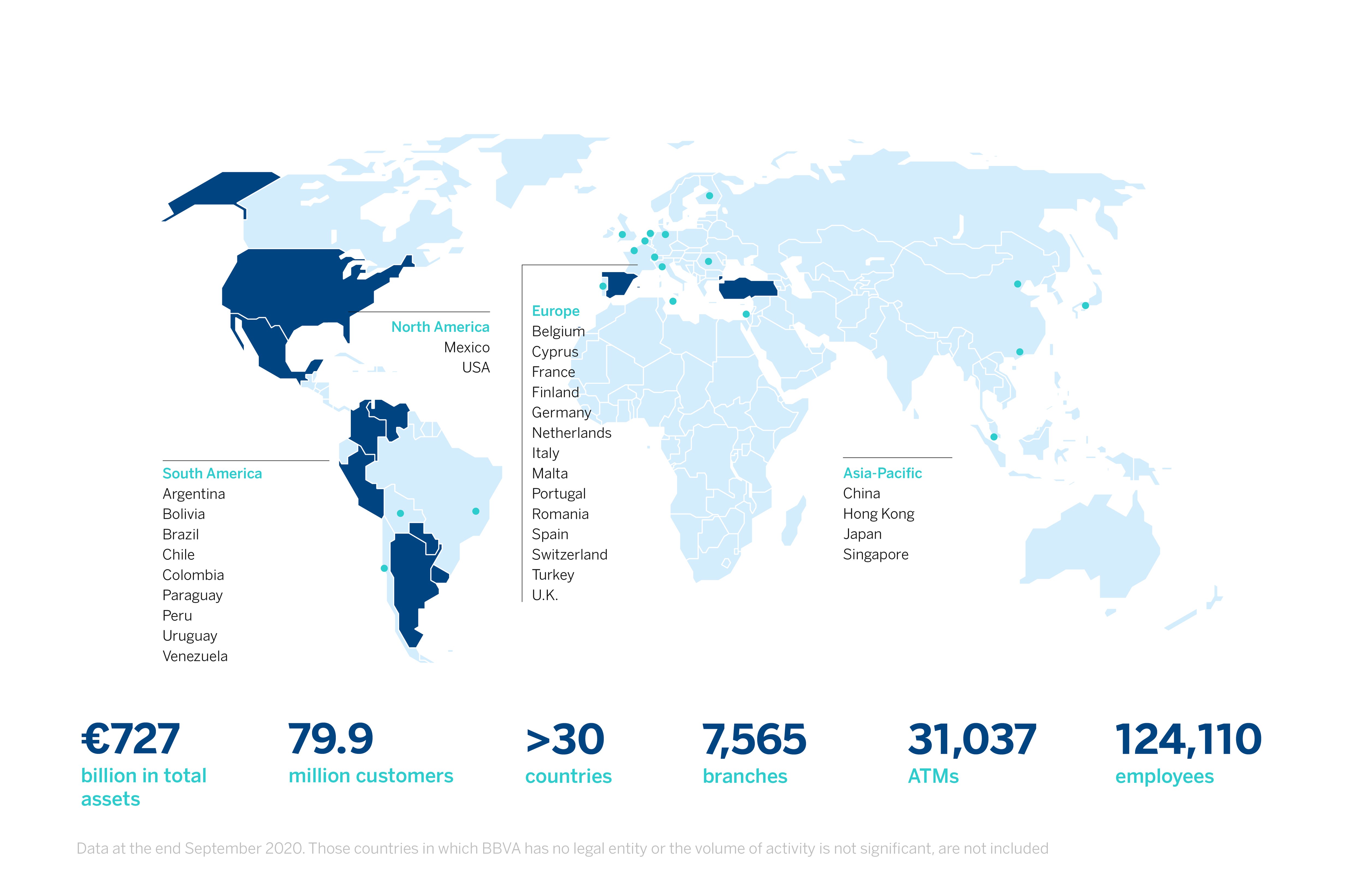

BBVA is a customer-centric global financial services group founded in 1857. The Group has a strong leadership position in the Spanish market, is the largest financial institution in Mexico, it has leading franchises in South America and the Sunbelt Region of the United States. It is also the leading shareholder in Turkey’s Garanti BBVA. Its purpose is to bring the age of opportunities to everyone, based on our customers’ real needs: provide the best solutions, helping them make the best financial decisions, through an easy and convenient experience. The institution rests in solid values: Customer comes first, we think big and we are one team. Its responsible banking model aspires to achieve a more inclusive and sustainable society.