BBVA earns €5.96 billion through September (+24 percent)

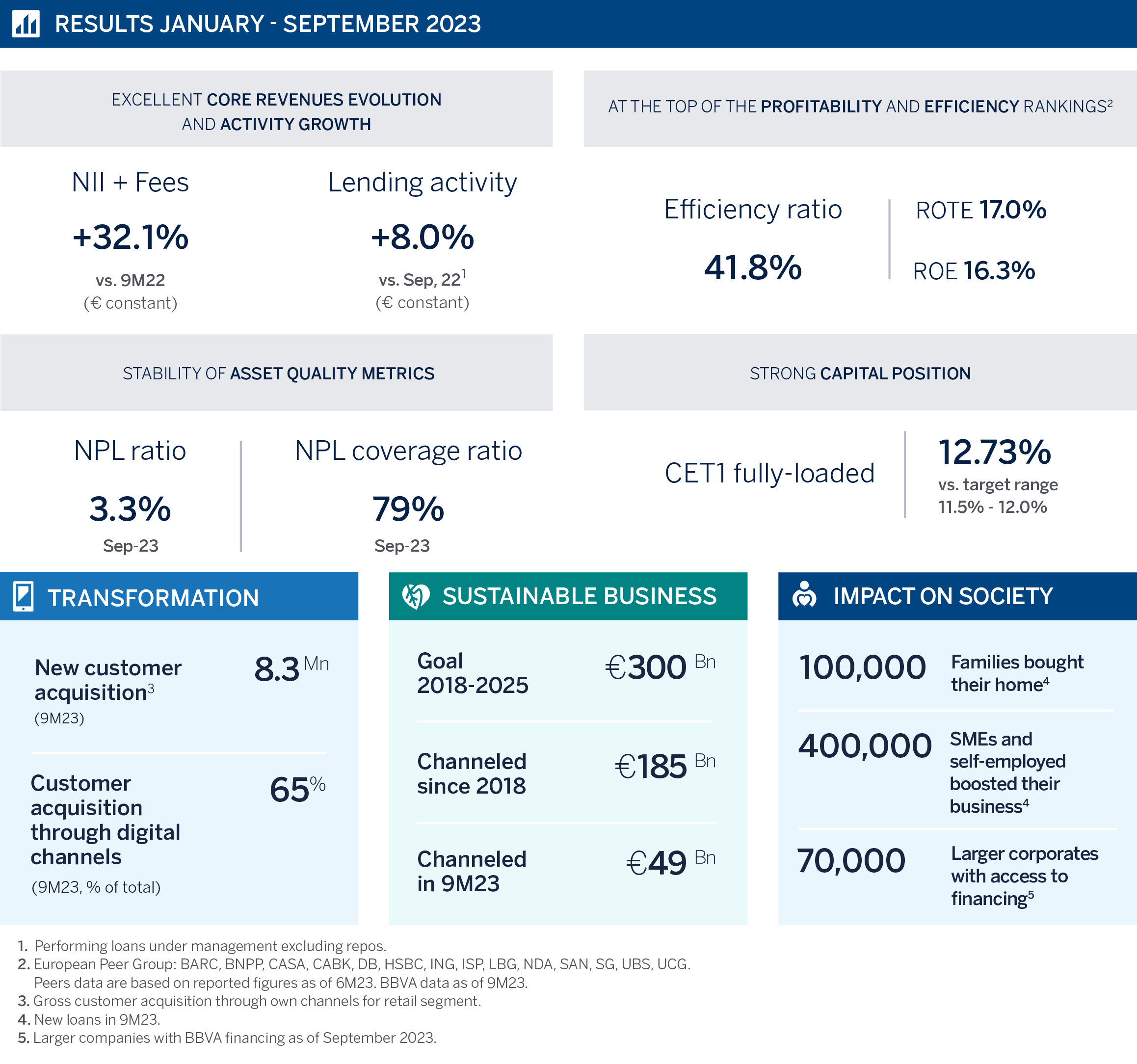

BBVA earnings showed a positive evolution in the first nine months of 2023. The Group posted a net attributable profit of €5.96 billion, up 24.3 percent yoy (+37.9 percent at constant exchange rates). These results were driven by the strong performance in recurring revenues (NII and net fees and commissions). This trend continued in the third quarter, with a net attributable profit of €2.08 billion, up 13.4 percent yoy. Earnings per share grew even higher, up 17.8 percent, thanks to the share buyback programs already executed by the bank. BBVA has a solid capital position, with a fully-loaded CET1 ratio of 12.73 percent, and ROTE reaching 17 percent.

Press kit Results 3Q2023

- Quarterly Report 3Q23 (PDF)

- Results Presentation Analysts 3Q23 (PDF)

- Download video (WeTransfer)

- Statement on BBVA 3Q23 earnings from Onur Genç (Text) (PDF)

- Statement from Onur Genç (YouTube)

- BBVA CEO Onur Genç (JPG)

- Ciudad BBVA (JPG)

- BBVA CEO Onur Genç and Global Head of Finance Luisa Gómez Bravo (JPG)

- BBVA CEO Onur Genç during the 3q23 results presentation (JPG)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

“We achieved excellent results in the first nine months of 2023 thanks to a strong performance in recurring revenue. We are one of the most efficient and profitable banks in Europe, with profitability that has already reached 17 percent. These results allow us to continue to create value for our stakeholders and contribute to the advancement of society as a whole.”

Greater activity boosted the loan portfolio by 8 percent over the past 12 months, allowing the bank to amplify the positive impact on society through financing to families and businesses. Specifically, it offered financing to 100,000 families to purchase their home, while helping 400,000 SMEs and the self-employed to grow their business. At the end of 3Q23, 70,000 large corporations had also received financing to foster their growth. Furthermore, BBVA allocated €12 billion to finance initiatives contributing to social inclusion, such as the construction of hospitals and schools, mortgages and social insurance, and financing to low-income customers.

Likewise, BBVA continues to make strides in its strategy for organic growth, based on innovation, digitization and sustainability. Between January and September, it added 8.3 million new customers, 65 percent of which joined the bank through digital channels.

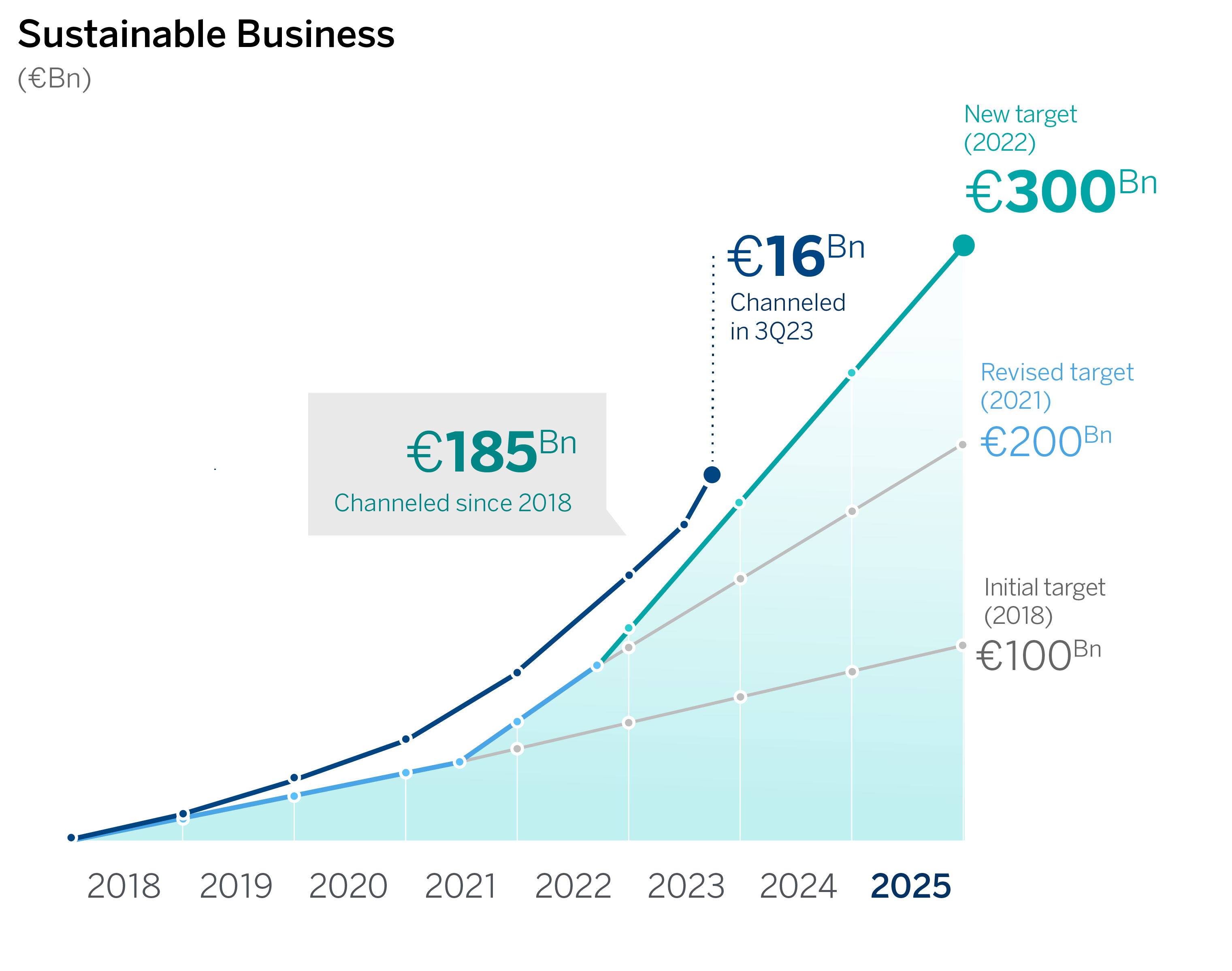

Regarding the bank’s commitment to sustainability, the Group has channeled €185 billion in sustainable business since 2018, devoting about 77 percent to climate change projects, and the remaining 23 percent to initiatives related to inclusive growth. In the first nine months of 2023, the bank channeled €49 billion, of which €16 billion took place in the 3Q23 alone (+13 percent yoy).

Except where otherwise stated, the evolution of each of the main headings, and changes in the income statement described below refer to constant exchange rates. In other words, they do not take currency fluctuations into account.

At the top of the P&L account, net interest income rose by 36.5 percent yoy, reaching €17.8 billion through September, with growth in all business areas on the back of improved customer spreads in the main business areas and higher performing loan volumes. Performance in Mexico, Spain and South America was particularly noteworthy.

Net fees and commissions or revenue for banking services reached €4.59 billion, 17.5 percent higher than last year’s figures, with a positive performance in all business areas, except Spain. NII and net fees and commissions, the bank’s core revenues, totaled €22.44 billion through September 2023, up 32.1 percent yoy. Furthermore, NTI contributed €1.43 billion, while the line for ‘other operating income and expenses’ posted an accumulated result of €-1.76 billion on the Group’s figures.

In total, gross income stood at €22.1 billion, up 31.8 percent yoy. Operating expenses grew 22.3 percent through September, to €9.24 billion, mainly due to high inflation rates in the Group’s footprint (an average of 18.1 percent over the past 12 months). Nevertheless, the strength of gross income secured positive jaws and an improvement in the efficiency ratio, which narrowed by 328 bps vs. the same period a year earlier, to 41.8 percent.

As a result of all the above, operating income rose 39.7 percent, to €12.86 billion, exceeding the €12 billion mark for the first time. At the end of September, impairments on financial assets stood at €3.2 billion, 35.5 percent higher than the previous year, mainly due to higher provisioning needs in South America and Mexico, amid higher interest rates and greater activity in the most profitable banking segments. Accordingly, the accumulated cost of risk in the first nine months of the year rose by 7 bps from June 2023 to 1.11 percent. The NPL ratio improved to 3.3 percent in 3Q23, and the coverage ratio fell slightly to 79 percent.

Between January and September 2023, BBVA posted a net attributable profit of €5.96 billion, up 37.9 percent compared to the same period the previous year (+24.3 percent in current euros). In 3Q23 the bank earned €2.08 billion, an increase of 29.6 percent yoy (+13.4 percent in current euros). Earnings per share rose even higher, to €0.33 (+17.8 percent in current euros) on the back of the share buyback programs that have already been executed.

BBVA continues to create value for its shareholders

Regarding profitability indicators, ROE and ROTE maintained their upward trend, reaching 16.3 percent and 17 percent, respectively, at the end of September. BBVA thus remains one of the most profitable European banks while continuing to create value for its shareholders: The tangible book value per share plus dividends increased by 18 percent in the past 12 months, to €8.6. These figures include the gross cash dividend of €0.16 per share that was paid in October against 2023 earnings, 33 percent higher than a year earlier. Furthermore, the Group is currently executing a €1 billion share buyback program, considered extraordinary shareholder distribution.

The fully-loaded CET 1 ratio stood at 12.73 percent as of September 30, 2023 - well above the bank’s target range of 11.5 to 12 percent.

Business areas

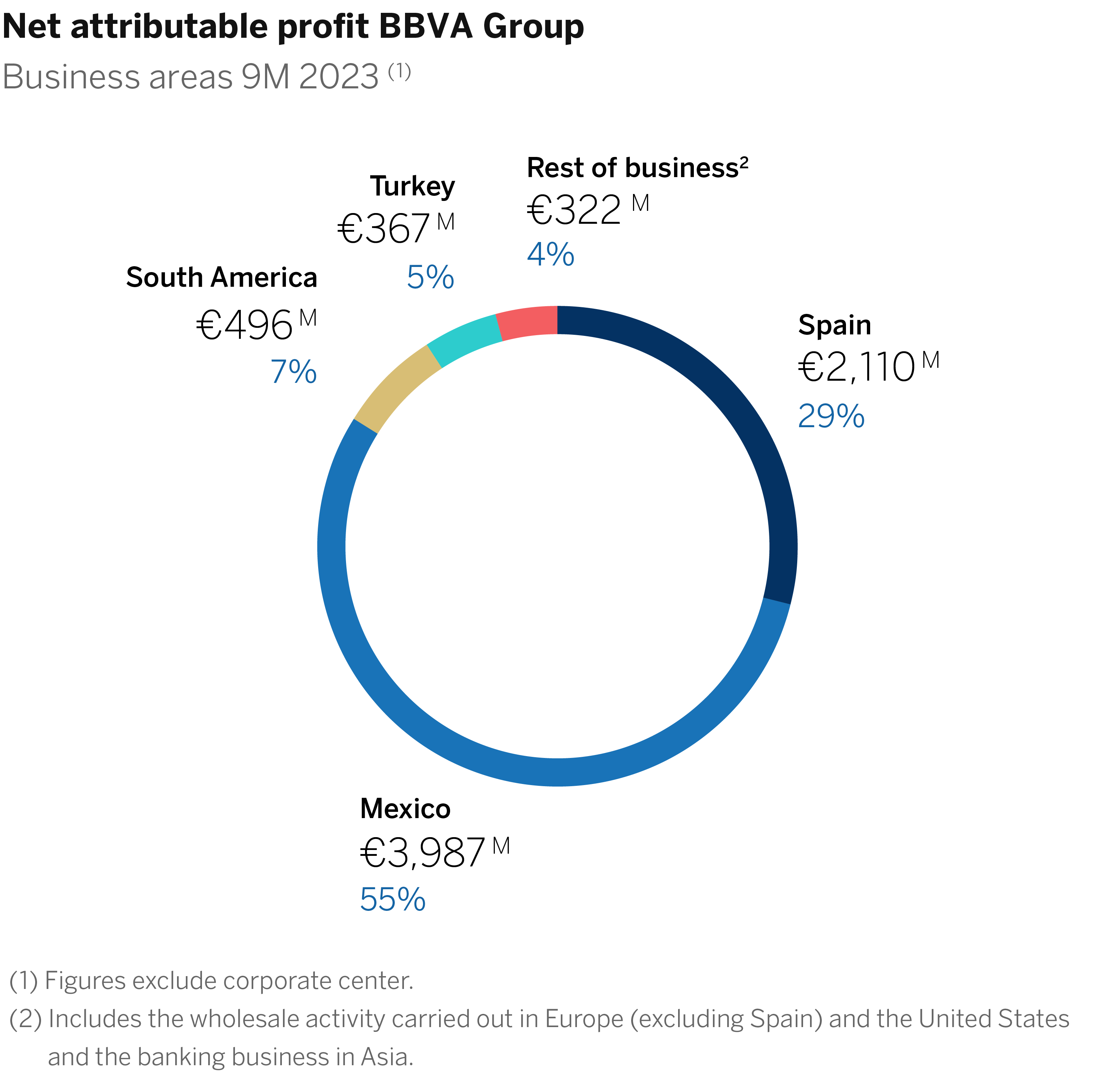

In Spain, lending activity fell 1.8 percent yoy, mainly due to mortgage cancellations made by some customers and deleveraging by large corporations, amid a context of higher interest rates. Greater activity in consumer loans, cards, public sector and SMEs helped offset this decline. Customer resources increased 2.2 percent yoy, driven by off-balance sheet funds growth. Between January and September, net attributable profit was €2.11 billion (+61.9 percent), including the impact of the extraordinary tax on banks (€215 million in 2023). The increase of NII (+50.8 percent) helped to increase gross income by 26.3 percent, prompting a notable improvement of the efficiency ratio, to 39.4 percent (-695 bps in the past 12 months). Regarding risk indicators, the NPL ratio in 3Q23 remained stable, around 4 percent, while the accumulated cost of risk increased slightly, in line with expectations, at very low levels (0.31 percent). The coverage ratio was 55 percent.

In Mexico, lending grew 11.2 percent yoy on the back of a good performance in all segments. Customer resources increased 11.7 percent, mainly driven by off-balance sheet resources. Net attributable profit topped €3.99 billion (+22.3 percent yoy), thanks to significant growth in NII (+23.3 percent), which continued to benefit from both greater lending activity and customer spreads. The increase in gross income also propelled improvement in the efficiency ratio, reaching 30.3 percent (-158 bps in the last 12 months). The NPL ratio stood at 2.6 percent (+8 bps vs. the previous quarter), and the coverage ratio was 127 percent. The accumulated cost of risk rose to 2.94 percent (+8 bps compared to the end of June), due in part to growth in the most profitable business segments, consumer loans and cards.

In Turkey, Garanti BBVA continued with the de-dollarization of its balance sheet as lending in Turkish lira increased 63.8 percent yoy, a much higher figure than that of loans in U.S. dollars (+5.3 percent yoy). Customer deposits in local currency also rose, by 126.4 percent yoy. Turkey posted a net attributable profit of €367 million through September. As for risk indicators, the easing of the NPL ratio stood out, continuing its descent in 3Q23 to 3.8 percent. This also led to improvement in the cost of risk, which slid to 0.26 percent. The coverage ratio stood at 100 percent.

In South America, lending improved by 10 percent yoy. Growth in retail portfolios in the region’s leading markets stood out as well as wholesale portfolios in Argentina and Colombia. As for customer resources, the region saw a relevant increase in time deposits, as well as demand deposits and mutual funds in Argentina. South America posted a net attributable profit of €496 million through September (+20.5 percent), driven by the positive evolution of recurring revenue. Risk indicators saw a slight deterioration due to the slowdown in economic growth. The NPL ratio stood at 4.6 percent, while the coverage ratio was 93 percent, and the accumulated cost of risk stood at 2.5 percent.

About BBVA

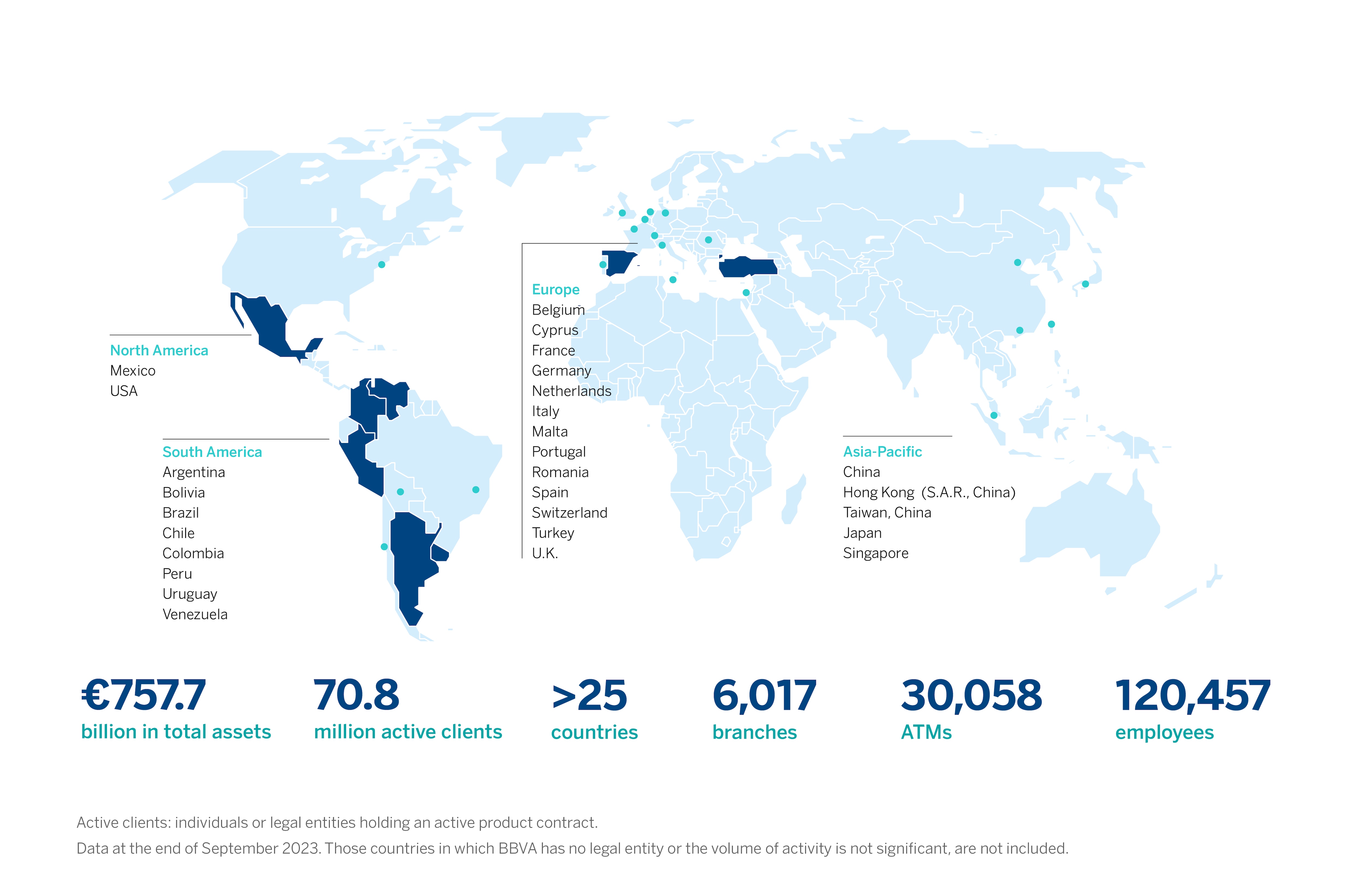

BBVA is a global financial services group founded in 1857. The bank is present in more than 25 countries, has a strong leadership position in the Spanish market, is the largest financial institution in Mexico and it has leading franchises in South America and Turkey. BBVA contributes with its activity to the progress and welfare of all its stakeholders: shareholders, clients, employees, providers and society in general. In this regard, BBVA supports families, entrepreneurs and companies in their plans, and helps them to take advantage of the opportunities provided by innovation and technology. Likewise, BBVA offers its customers a unique value proposition, leveraged on technology and data, helping them improve their financial health with personalized information on financial decision-making.