Startups in a post-coronavirus world: how will the crisis impact fintech?

The coronavirus crisis may lead to a series of changes forcing many companies to rethink their business models. Startups frequently depend on funding, and some may be critically impacted. Still, others may find themselves in a stronger position thanks to their capacity to adapt to the changing landscape or because they provide digital services that have proven invaluable. Could the coronavirus crisis set the stage for the next big startup?

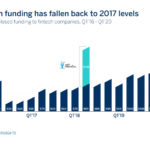

“Funding conditions have undergone a 180 degree shift, and the future of fintech has changed dramatically,” market intelligence company CB Insights asserts in a recent report on the current crisis’ impact on global venture capital funding for financial technology companies. According to data collected by the consulting firm, the volume of funding rounds for the fintech sector has fallen 45 percent compared to Q4 2019, and 25 percent compared to the same period last year. CB Insights postulates that if fintech funding continues at this pace, it will reach approximately $6 billion (circa €5.53 billion) in the first quarter of 2020, its lowest level since 2017.

Chasing profitability

What impact will this have on the sector? “Companies will have to tighten their belts, and focus more on profitability and positive cash flow than growth at all costs,” the report explains. According to the consulting firm, this represents a marked change from the last decade when some fintech companies were able to raise enormous amounts of capital even without demonstrating profitability.

Datos de las rondas financiación anunciadas en compañías 'fintech' entre 2016 y 2020. - CB Insights

“It is true that in the last few years there has been some hype around specific fintech business models that were not yet profitable; and now they’ll have to get used to working with less money, just like everyone else,” Gustavo Vinacua, BBVA’s Head of Venture Creation, agrees. “And this probably forces many startups to rethink their strategies, to look at their more robust lines of business and set aside other innovative projects that haven't yet demonstrated profitability or are less a sure thing, still in an exploratory phase. Like most businesses today, fintechs will have to be more efficient,” he adds.

"It's extremely likely that the next startup to hit the big time will be related to some kind of new behavior that has come to the fore during the crisis”

Some of the more established technology startups have already been forced to take steps: Last week Uber announced it would be reducing its workforce by 14 percent, and AirBnB announced a 25 percent cut. In both cases, the companies explained that they will be closing their most disruptive lines of business (Uber’s flying taxis, for example) in order to focus on their core business.

Being agile to embrace change

A company’s ability to rapidly make changes in response to a changing landscape is precisely the advantage emerging startups have in the face of a crisis like the current one. “Startups are more adept at pivoting quickly, shutting down projects, reorienting themselves toward real profits, and even turning their business model on its head. They are more resilient to change than large companies, and this plays to their favor in times like these,” Vinacua adds.

For example, faced with the coronavirus-induced drop in funding, U.S. neobank Moven recently announced that it has decided to sell its direct consumer offering in order to focus exclusively on developing financial technology for other banks. There are also examples of fintech startups that have quickly launched new products or solutions in response to the current environment. For example, the U.S. digital bank, Chime, launched an online solution to deliver advance payments of government-issued economic aid in response to the COVID-19 crisis. Then there is Credit Kudos, a British startup credit rating agency specializing in the use of open banking data. They have launched a tool targeting freelancers that lets them quickly verify their earnings, helping them benefit from British government handouts.

Online is in the genes

Another factor that might help these kinds of companies weather the crisis is their limited operational dependence on brick and mortar offices. “These companies have the advantage of already having decentralized teams, so remote working isn't anything new. This means they are less vulnerable to the changes produced with the pandemic: doing without an office is not a hardship and their business models had already accommodated 100 percent online channels,” Vinacua explains.

In this respect, the crisis could even act to strengthen some fintech companies’ business models, those whose services may be more relevant than ever, like companies specializing in digital payment solutions or online sales platforms. “This could have an especially significant impact in areas where there is still a long way to go in online payments. For example, in Latin America the crisis could act as an impetus to the wider-scale adoption of digital payment solutions that have seen less penetration,” BBVA’s executive explains.

In general, the impact on fintechs will be varied, with marked differences by sector. “Logically, startups that are more closely linked to industries like tourism or entertainment will suffer the most, but those dedicated to online banking, like some of the neobanks, or to payment solutions and ecommerce, could weather the crisis better,” he points out.

Blue oceans

The crisis resulting from the COVID-19 pandemic, like previous economic downturns, could create specific business opportunities emerging from new, unanswered needs that will become more evident in the post-crisis landscape. “I think a lot of the trends we see today, like remote working, are here to stay, and it's extremely likely that the next startup to hit the big time will be related to some kind of new behavior that has come to the fore during the crisis,” Vinacua explains.

Vinacua has led research conducted in the past few weeks analyzing what opportunities could emerge in the changed environment. Among the trends identified, Vinacua calls attention to opportunities he thinks will emerge around cooperative-based models with companies sharing assets, resources, and even workspaces, thus creating business ecosystems that are more resilient to change.

"Our sense of solidarity and collaborative approach to looking for solutions to the problems we are facing will continue to be reflected in the kinds of initiatives that emerge in the future”

One such example is aggregate purchasing, where different companies partner so they can buy more cheaply and pass their savings on to their customers. “This is something that has been commonplace for decades among Asian companies, and to a lesser extent in Europe, but given the current situation it could become a popular approach in other regions, even being adopted by small businesses,” he explains. Along these lines, Vinacua also indicates that in the near term, it is possible we’ll see a greater proliferation of solutions focused on helping small companies withstand the repercussions of the crisis. “Solutions will emerge to help businesses that don’t have their own online sales channel infrastructure,and companies that have never needed digital tools will adopt them,” he adds.

According to Vinacua, being able to pivot like a startup will also become an essential asset in dealing with the post-crisis environment, not only for young businesses, but also for large corporations. “And this will be another area where opportunities arise: enabling large companies to use their assets in different ways, to adapt to a new situation,” he adds.

It is Vinacua’s view that in the future global supply chains will also undergo change, striving to be more resilient. This is an area where new needs will create new business models. “There will be a trend to make supply changes more local, regional, or national so they are not threatened by an interruption caused by this type of crisis. In other words, creating stronger, more resilient supply chains that are better placed to weather adverse impacts,” Vinacua says.

“Finally, it seems as if our sense of solidarity and collaborative approach to looking for solutions to the problems we are facing will continue to be reflected in the kinds of initiatives that emerge in the future,” he concludes.