BBVA posts net attributable profit of €3 billion in first half of 2022

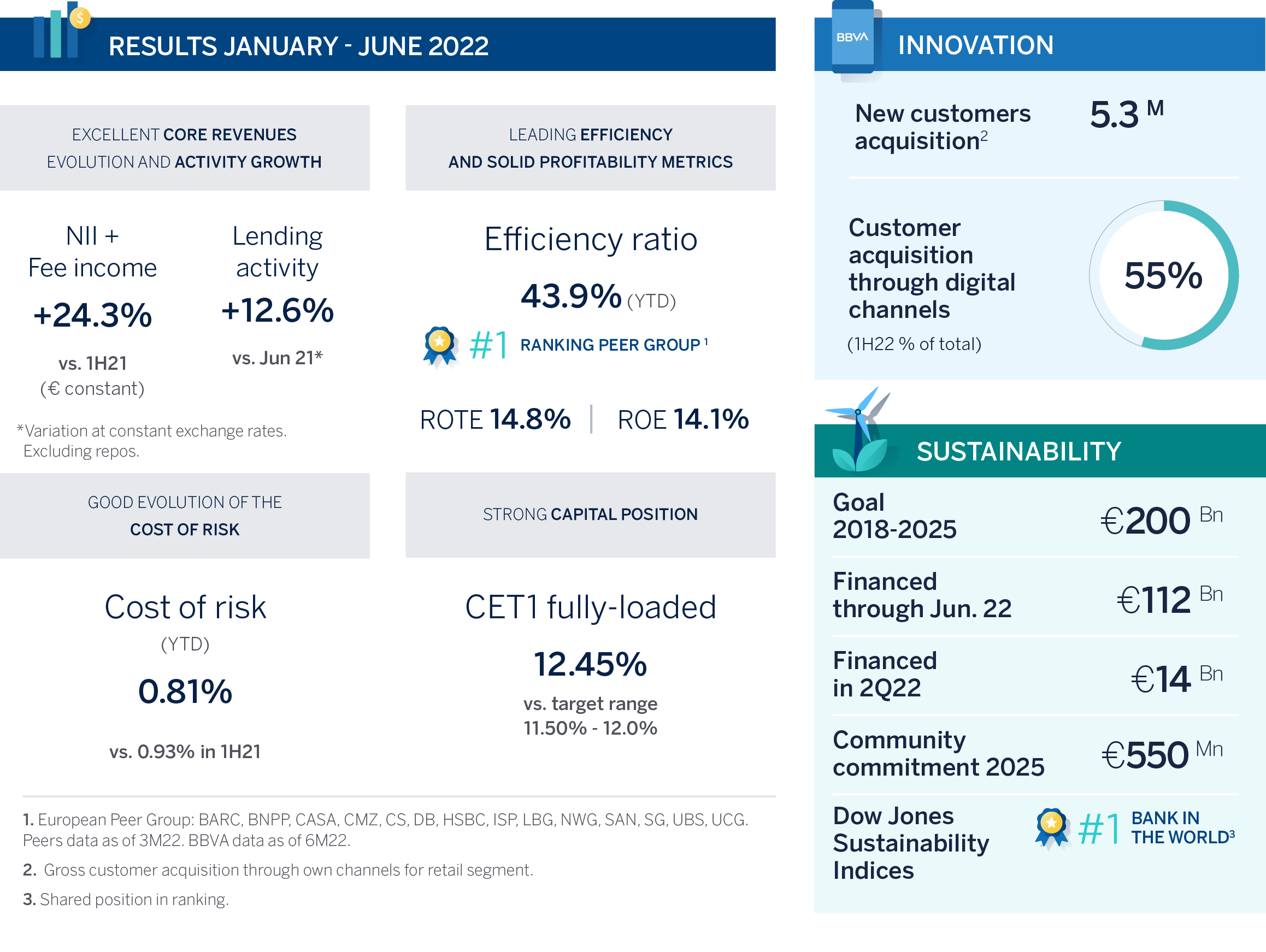

The BBVA Group posted a net attributable profit of €3 billion in the first half of 2022 (+59.3 percent yoy in constant euros, +57.1 percent at current exchange rates), on the back of strong revenues, driven by greater activity (+12.6 percent), lower provisions and appropriate cost management in an environment of high inflation. Excluding the non-recurring impact from the acquisition of offices in Spain from Merlin, recurrent profit totaled €3.2 billion (+40.8 percent in constant euros, +37.6 percent at current exchange rates). BBVA also set a new quarterly record in terms of customer acquisition and sustainable financing.

“In the second quarter of 2022, we achieved strong results thanks to the positive performance of revenues, driven by the growth in activity and a good evolution of risk indicators. These results allow us to accelerate the creation of value for our shareholders, and to be the most efficient, and one of the most profitable banks in Europe. We have helped our customers with an increase in loans in all geographies, quarter after quarter, reaching double-digit growth rates,” BBVA CEO Onur Genç said.

Except where otherwise stated, in order to better understand the evolution of each of the main headings, changes in the income statement described below refer to constant exchange rates. In other words, they do not take currency fluctuations into account. Additionally, figures for Turkey starting January 1, 2022, are under hyperinflationary accounting.

Net interest income (NII) reached €8.55 billion in 1H22, up 26.5 percent yoy, driven by solid activity growth. A solid performance in Mexico, Turkey and South America helped offset NII stability in Spain. Net fees and commissions increased 17.8 percent to €2.65 billion, with good performance in the main countries, thanks to higher activity. On the whole, recurring revenues (NII + fees and commissions) grew 24.3 percent, reaching €11.2 billion. Net trading income (NTI) increased 5.5 percent yoy to €1.1 billion, mainly driven by the contribution of the Global Markets unit in Spain and Turkey.

The line referring to ‘other operating income and expenses’ accumulated a negative result of €787 million as of June 30, 2022. This is primarily the result of the adjustment for inflation in Turkey since Jan. 1, 2022.

Gross income rose 15.8 percent to €11.51 billion, and operating expenses (+12 percent) grew below the average inflation rate in the countries where BBVA operates (+13.1 percent). These two factors resulted in positive jaws. The efficiency ratio stood at 43.9 percent at the end of June - the best among European peers.

As a result, operating income reached €6.46 billion in 1H22, up 19 percent yoy.

The lines of ‘impairments on financial assets and provisions’ and ‘other results’ both fell 9.1 percent and 57.1 percent, respectively, compared to 1H21. The cumulative cost of risk remained at the same level as 1Q22: 0.81 percent, with a better than expected performance. The NPL ratio improved once again from 3.9 percent to 3.7 percent. The NPL coverage ratio increased from 76 to 78 percent.

The BBVA Group posted a net attributable profit of €3 billion in 1H22, up 59.3 percent yoy. Excluding the net impact of €-201 million of the acquisition of offices in Spain from Merlin, the recurrent profit stood at €3.2 billion, up 40.8 percent. In 2Q22, the bank’s profit reached €1.68 billion.

BBVA continues to be one of Europe’s most profitable banks, with ROE and ROTE of 14.1 and 14.8 percent, respectively. BBVA also created value for its shareholders. The tangible book value per share plus dividends stood at €7.5, up 18.4 percent yoy.

As for activity, it is worth noting the strong growth in loans¹, which has accelerated quarter after quarter, reaching 12.6 percent yoy at the end of June 2022.

The Group’s fully-loaded CET1 ratio stood at a solid 12.45 percent, above the target range of 11.5 to 12 percent. This ratio includes the impact of operations carried out in the second quarter, with a total impact of -30 basis points. (These operations include the voluntary takeover bid for Garanti BBVA and the acquisition of 662 offices from Merlin and rented to BBVA).

New record in customer acquisition and sustainable financing

Digitization has multiplied by 2.7 times the pace of customer acquisition compared to five years ago. In 1H22, BBVA posted a record number of new customers: 5.3 million, 55 percent of which joined the bank via digital channels (compared to 6 percent just five years ago). Furthermore, the Group’s customers show increasingly a stronger engagement with the bank: i.e. 72 percent of new customers in Spain become target customers in just six months².

The bank currently has 45.5 million digital customers, representing 71.4 percent of the total, while mobile customers stand at 43.5 million, accounting for 68.1 percent of the total. Digital sales represent 76.7 percent of total units sold.

Progress has also been significant in sustainable financing. In 2Q22, the bank financed more than €14 billion - up 50 percent compared to the same quarter the previous year, and a new record. BBVA has financed €112 billion between 2018 and June 2022, surpassing the halfway point of its Goal 2025.

Business areas

In Spain, lending rose 3.6 percent yoy, mainly due to growth in the most profitable segments: Corporate and CIB and other commercial, together with consumer loans and cards. Customer funds increased 3 percent yoy, with solid growth in demand deposits (+10.3 percent). This helped offset the drop in time deposits (-30.8 percent), and off-balance sheet funds (-2.4 percent). Spain posted a net attributable profit of €808 million in 1H22, up 11.5 percent yoy, on the back of higher activity, a significant improvement in efficiency and lower impairments on financial assets. Excluding the net impact of €201 million for the acquisition of offices from Merlin, profit rose to €1.01 billion. In terms of risk indicators, the NPL ratio improved from 4.2 percent to 4 percent in the quarter. The NPL coverage ratio remained stable at 62 percent. The cost of risk was better than expected, standing at 0.2 percent in cumulative terms.

In Mexico, lending activity posted a 13.3 percent gain yoy, with improvement in all segments. Customer funds rose 10.2 percent, driven by positive evolution of all lines. Net attributable profit in Mexico stood at €1.82 billion in 1H22, up 48.3 percent compared to the same period the previous year. This was the result of good performance in recurring revenues, particularly favored by the evolution of NII, positive jaws, and contained loan-loss provisions. In 2Q22, net attributable profit stood at a record €1.01 billion. Risk indicators also improved in 2Q22: The NPL ratio ended at 2.8 percent, from 3 percent, while the NPL coverage ratio improved from 115 percent to 119 percent. The cumulative cost of risk improved by 27 bps vs 1Q22, reaching 2.57 percent, with a better than expected performance.

In Turkey, lending in Turkish lira grew 54.1 percent yoy, mostly thanks to momentum in the retail and commercial segments compared to a 12.3 percent drop in loans in U.S. dollars. This loan portfolio has been shrinking since 2015 as part of a prudent risk management strategy. Customer deposits in Turkish lira increased 61.3 percent yoy. Turkey posted a net attributable profit of €62 million in 1H22. This figure includes the impact from hyperinflationary accounting, applicable as of January 1, 2022. This negative impact was partially offset by income from inflation-linked bonds (CPI linkers) registered under the line ‘other operating income and expenses’. It should be pointed out that this area’s net attributable profit considers a stake of 85.97 percent in Garanti BBVA following the completion of the voluntary takeover bid on May 18, 2022 (compared to a 49.85 percent stake owned by BBVA before the takeover bid). As for risk indicators, the NPL ratio improved from 6.7 percent in 1Q22 to 5.9 percent. The NPL coverage ratio rose from 75 percent to 83 percent, and the cost of risk improved from 0.99 percent to 0.88 percent.

In South America, the loan portfolio saw an increase of 12.1 percent yoy, with growth in all segments. Customer funds rose 11.8 percent. South America earned €413 million in 1H22 (+102.1 percent yoy), thanks to a good performance of recurring income and lower loan-loss provisions, which comfortably helped offset growth in operating expenses amid an environment with high inflation throughout the region. Colombia contributed €149 million; Peru earned €117 million, and Argentina, €101 million. The NPL ratio stood at 4.2 percent, which represents an improvement of 13 bps in 2Q22, with reductions in Colombia and Argentina. The NPL coverage ratio was 100 percent. The cumulative cost of risk stood at 1.24 percent, better than expected.

¹Performing loans under management excluding repos.

²Target customers refers to those customers in which the bank wants to grow and retain, as they are considered valuable due to their assets, liabilities and/or transactionality with BBVA.

About BBVA

BBVA is a customer-centric global financial services group founded in 1857. The Group has a strong leadership position in the Spanish market, is the largest financial institution in Mexico and it has leading franchises in South America. It is also the leading shareholder in Turkey’s Garanti BBVA and has an important investment, transactional and capital markets banking business in the U.S. Its purpose is to bring the age of opportunities to everyone, based on our customers’ real needs: provide the best solutions, helping them make the best financial decisions, through an easy and convenient experience. The institution rests in solid values: Customer comes first, we think big and we are one team. Its responsible banking model aspires to achieve a more inclusive and sustainable society.