BBVA earns €3.31 billion through September, proceeds with one of the largest share buybacks in Europe

BBVA Group posted a net attributable profit of €3.31 billion between January and September 2021, compared to a €15 million loss a year earlier. The recurring profit¹ stood at €3.73 billion, up 85 percent from last year. In 3Q21 alone, the attributable profit was €1.4 billion, one of the highest in record. These earnings were possible thanks to the solid performance of the net interest income and fees and commissions, and a better-than-expected evolution of impairments. The Group maintained its solid capital generation capacity (+31 basis points since June), with a fully-loaded CET1 ratio of 14.48 percent at the end of September. This capital strength allows BBVA to carry out a share buyback of up to 10 percent of its share capital, for a maximum amount of €3.5 billion.

Press kit Results 3Q21

- Quarterly Report 3Q21 (PDF)

- Statement on BBVA 3Q21 earnings from BBVA CEO (Text) (PDF)

- Statements from Onur Genç (YouTube)

- 3Q21 Results Presentation - Press (PDF)

- Statements from Onur Genç - TV Spanish (WeTransfer)

- Results Presentation Analysts – 3Q21 (PDF)

- Download audio (WeTransfer) (Radio)

- 'La Vela', main building in 'Ciudad BBVA' (JPG)

{kind=link}

“Our results have shown an excellent evolution in the third quarter of 2021. The net attributable profit reached €1.4 billion on the back of strong core revenue growth, and solid underlying risk performance. The capital strength allows us to continue growing and to increase our shareholders distributions. In this sense, the European Central Bank has authorized the share buyback plan of up to 10 percent of our shares with a maximum size of €3.5 billion, one of the largest in Europe to date,” BBVA CEO Onur Genç said.

BBVA’s third-quarter figures maintained the recovery trend started in the previous quarter, driven by the good behavior of recurring revenues (net interest income and fees and commissions) and an improvement of risk indicators.

Except where otherwise stated, to better understand the changes under the main headings of the Group's income statement, the yoy percentage changes provided below refer to constant exchange rates, i.e. not taking into account currency fluctuations.

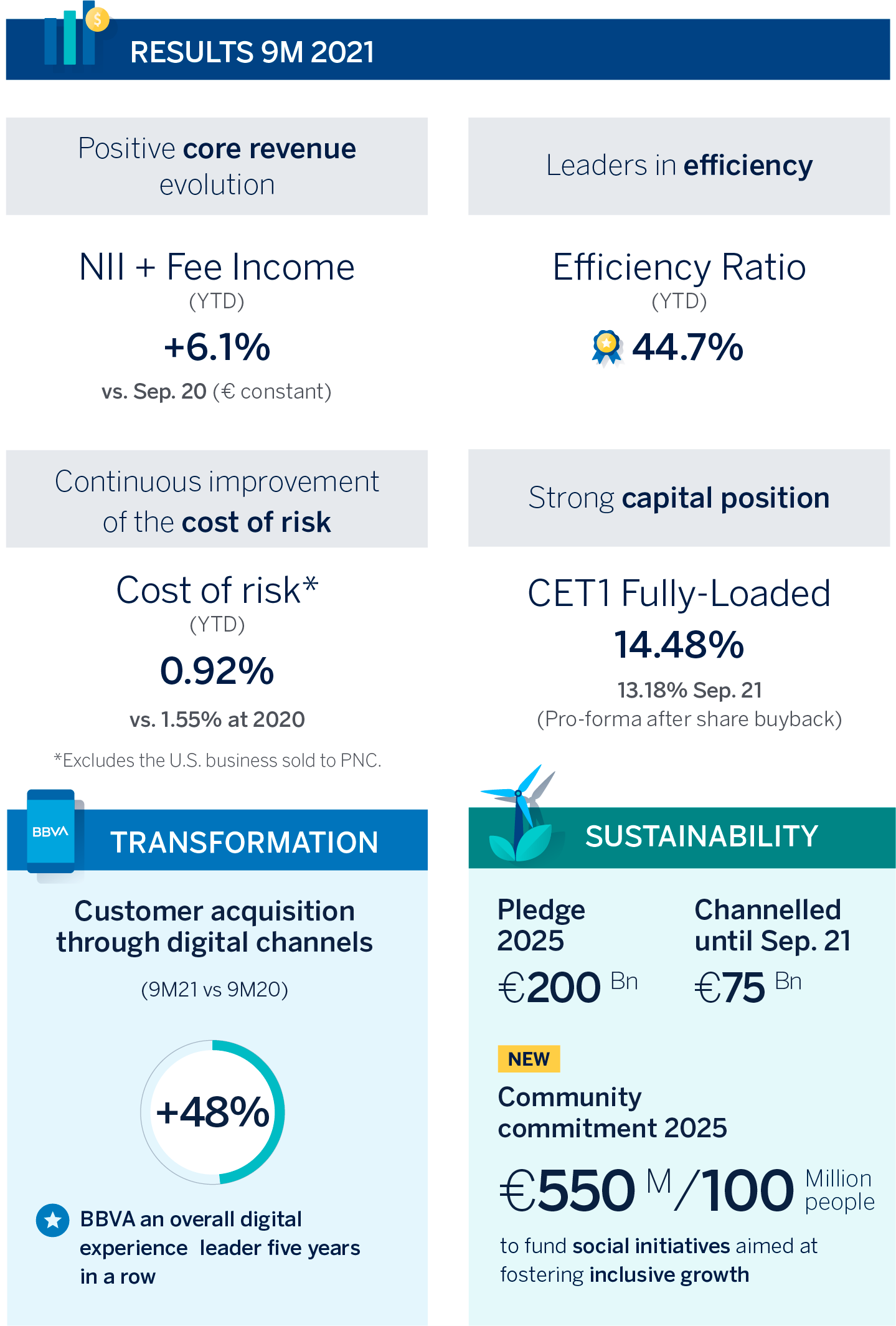

On the top of the income statement, net interest income (NII) grew 2.5 percent yoy, to €10.71 billion between January and September 2021. The quarterly performance confirmed the Group’s expectations regarding both the upbeat prospects and uptick in the growth rate of this heading throughout the year (it grew 6.1 percent in 3Q21, compared to a 3.9 percent growth in 2Q21). Net fees and commissions maintained the strength shown in 1H21 and grew 19.2 percent yoy in the first nine months, to €3.52 billion. Overall, NII plus fees and commissions – which make up the recurring revenues of the banking business – grew 6.1 percent yoy, to €14.23 billion.

Net Trading Income (NTI) stood at a solid €1.47 billion through September (+13.7 percent yoy), driven by the solid performance of the Global Markets Unit in Spain and the revaluations of the Group’s stakes in Funds & Investment vehicles in tech companies and its industrial and financial portfolio.

As a result, gross income grew 5.6 percent yoy between January and September to €15.59 billion.

Operating expenses increased 6.5 percent through September to €6.98 billion, in a context of widespread economic growth, and activity returning to normal levels. Compared to the same period in 2019, a pre-COVID year, expenses increased 3.4 percent. BBVA remains the leader in efficiency of its EU comparable peer group. The efficiency ratio in September stood at 44.7 percent, improving 83 basis points since the end of 2020.

The operating income for the first nine months of the year stood at €8.61 billion, up 4.9 percent from the previous year.

During the first nine months of 2021, it is also worth noting the sharp decline in impairments on financial assets (-46.2 percent) thanks to a solid underlying risk performance -in line or better than in pre-pandemic levels-, as well as provisions and other results (-72.7 percent).

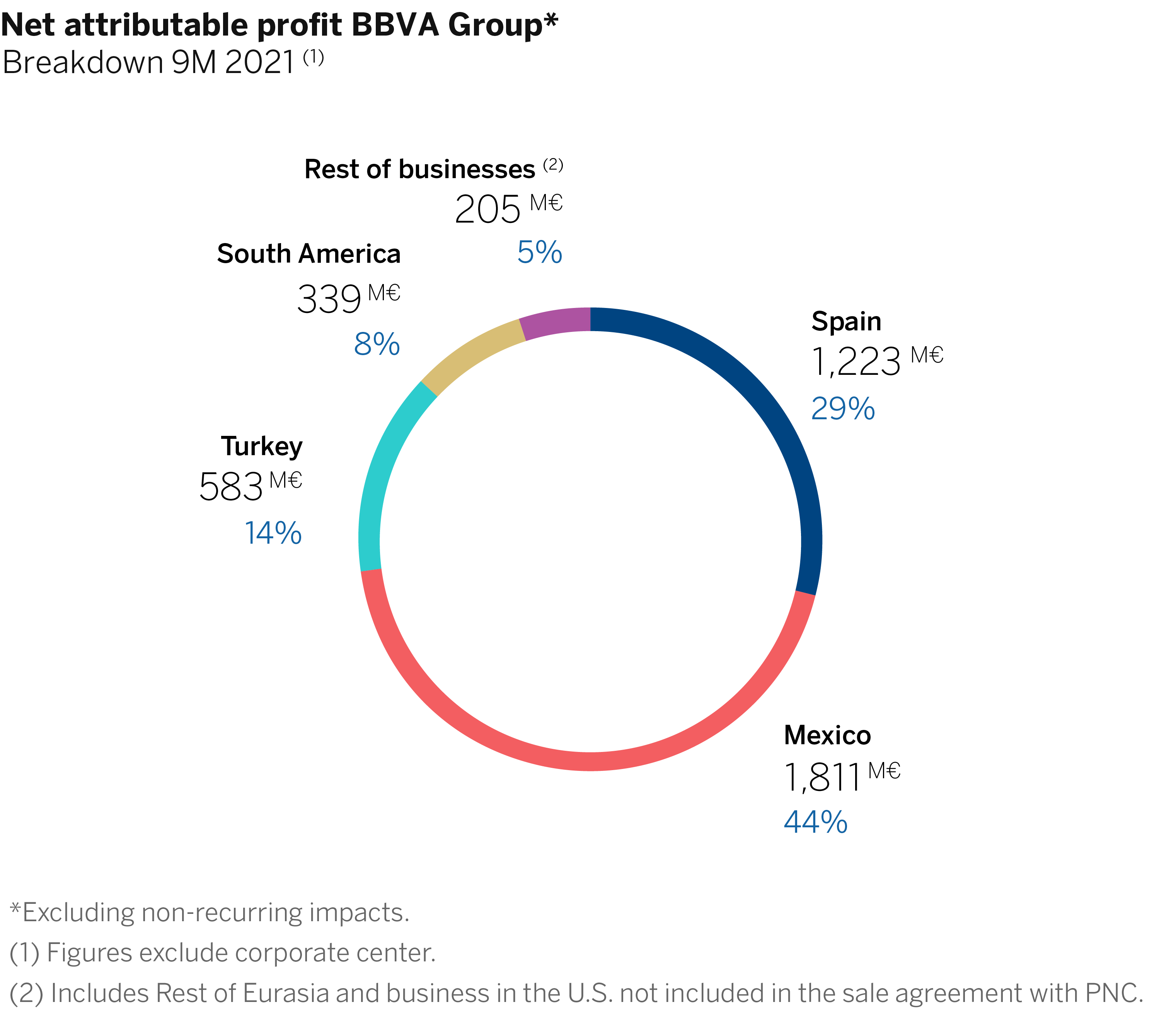

The BBVA Group’s attributable profit reached €3.73 billion between January and September, excluding non-recurring impacts. This figure virtually doubles the recurring revenue of the first nine months of 2020.

The non-recurring impacts are the €280 million profit posted by BBVA USA and other related businesses through June 1, 2021, which were then sold to PNC; and the €-696 million in net costs linked to the restructuring process in Spain. Including both impacts, the attributable profit stood at €3.31 billion for the first nine months, compared to a loss recorded in the same period of the previous year, heavily impacted by the pandemic.

The Group’s profitability indicators also improved, in line with the attributable profit’s performance: ROE stood at 11.1 percent² and ROTE at 11.7 percent, compared to 10.4 percent and 11 percent in 1H21.

As for capital, the Group’s fully-loaded CET1 ratio stood at 14.48 percent as of September 30, 2021, a figure that is comfortably above (588 bps) the regulatory requirements. BBVA has also received the authorization from the ECB to proceed with a share buyback plan of up to 10 percent of its share capital for a maximum amount of €3.5 billion³. This plan is one of the largest in Europe to date. The buyback will be executed in several tranches during a maximum period of 12 months. The first one, which will be for a maximum of €1.5 billion⁴ and an expected time frame of execution of three to four months, will start following BBVA’s Investor Day (Nov. 18, 2021). The pro-forma CET1 ratio, excluding the maximum amount of the €3.5 billion share buyback plan, would stand at 13.18 percent⁵.

Additionally, on October 12, 2021, BBVA paid a cash interim dividend of €0.08 (gross) per share against 2021 results. All in all, BBVA remains committed to creating value for its shareholders.

The tangible book value per share plus dividends stood at €6.55 at the end of September (+12.3 percent yoy).

Regarding risk indicators, it is worth noting that the cumulative cost of risk declined to 0.92 percent (compared to 1.68 percent a year earlier and 1.00 percent from the previous quarter), beating expectations. The NPL ratio improved to 4 percent compared to June, while the NPL coverage ratio rose to 80 percent. These figures exclude the balances corresponding to the business in the United States, sold to PNC.

As for balance sheet and activity, the gross figure for loans and advances to customers grew 1.5 percent vs. the end of 2020, driven mainly by growth among retail customers (+2.5 percent) across virtually the entire footprint. Customer funds also increased 1.5 percent vs. 2020 year-end, driven by the positive trends in demand deposits and off-balance sheet funds across all geographies (especially mutual funds in Spain and Mexico).

New record in digital customer acquisition

Figures through September 2021 confirmed that the pandemic dramatically increased the use of digital channels among customers. The Group added close to 2.5 million new customers through digital channels (up 48 percent yoy), a new all-time high. Digital customers account for 68 percent of the total, with 40.1 million (+36 percent since September 2019). Mobile customers have grown by 43 percent over the past two years, to 37.9 million, and account for 64 percent of the Group’s customer base. Digital sales now represent 72 percent of all units sold.

For five years in a row, BBVA has been named Europe’s leader in digital experience according to ‘The Forrester Digital Experience Review™: European Mobile Banking Apps, Q321’ report.

Finally, the Group recently announced the launch of a fully digital retail offering in Italy, with a unique value proposition and customer experience.

New commitment to sustainability

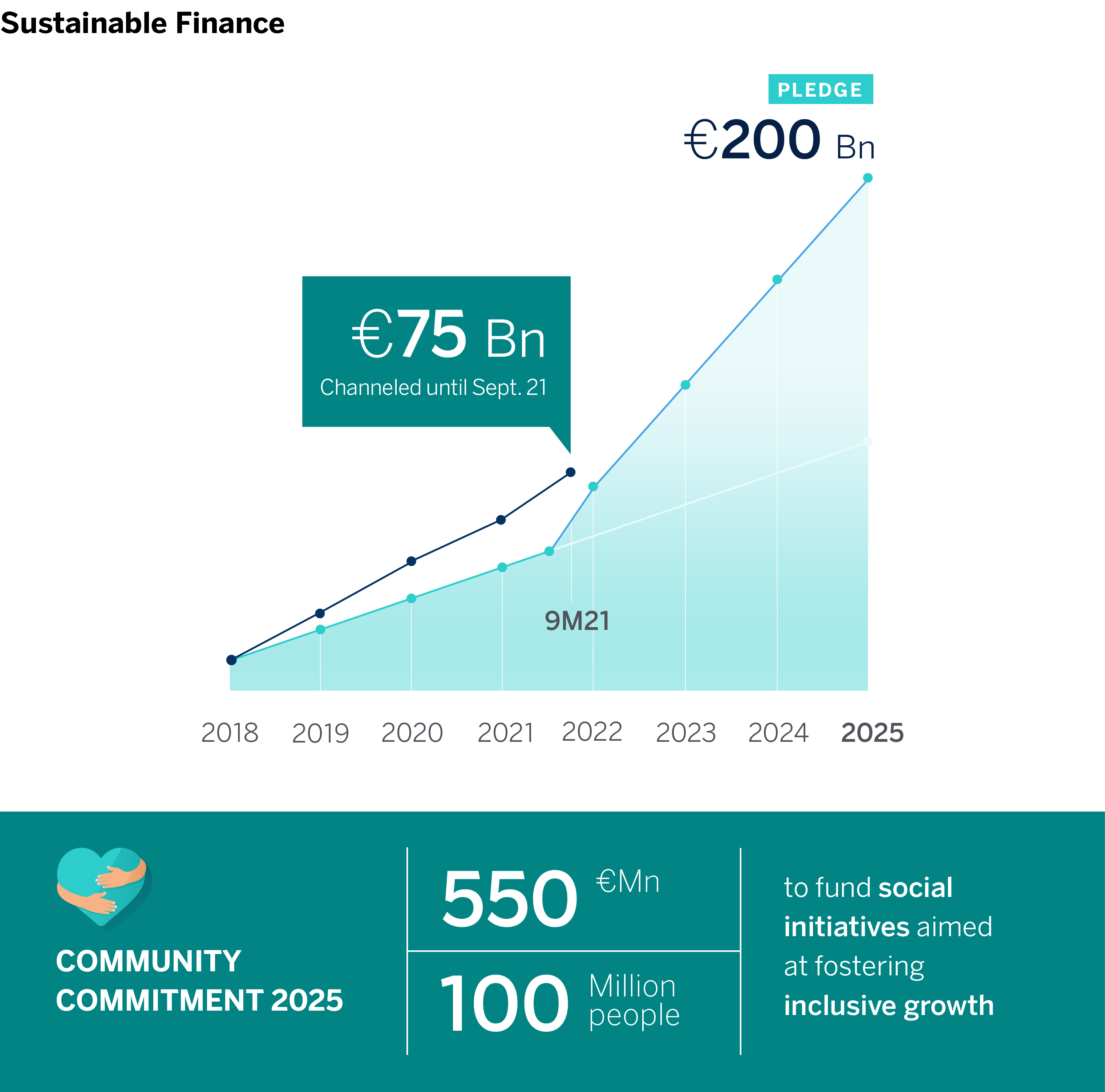

BBVA continued working towards delivering on its pledge to channel €200 billion in sustainable financing through 2025. As of September 2021, it had already originated €75 billion, €8 billion in 3Q21 alone. The Group keeps launching innovative solutions to help its customers in their transition to a more sustainable future.

The bank has recently made available to clients in Spain its carbon footprint calculator, already presented in its version for businesses in 2020.

BBVA is also making progress in its Net Zero 2050 Commitment. Following the announcement in March of the phase-out plan for coal, the Group has defined new decarbonization targets by 2030 in some carbon-intensive sectors.

This information will be presented as part of the COP26 event.

The Group recently announced a new social inclusion commitment. BBVA and its foundations will devote a total of €550 million during the 2021-2025 period to fund social initiatives aimed at fostering inclusive growth in its footprint.

This commitment will be materialized along three lines of action, aligned with the UN Sustainable Development Goals: reducing inequality and promoting entrepreneurship; creating opportunities through education; and supporting research and culture.

Business areas

The solid performance in recurring income, positive NTI trends (except in Mexico) and lower impairments on financial assets and provisions explain, to a large extent, the relevant growth of attributable profit by the Group’s key business areas. These factors also explain the significant drop in the cumulative cost of risk across virtually all geographies, after its peak in 1Q20.

In Spain, the loan portfolio increased by 1.1 percent as of the end of September yoy, thanks to the solid growth rates in consumer finance and mid-sized companies. In the P&L account, net interest income decreased 1.9 percent yoy between January and September, although the strength of the income from net fees and commissions (+18 percent) during the period drove recurring revenues to grow by 4.7 percent. Compared to 2Q21, fees and commissions decreased by 3.1 percent in 3Q21. Gross income grew 3.6 percent while the operating income increased 9.2 percent compared to the first nine months of 2020, driven also by cost discipline

(-1.7 percent). Net attributable profit through September stood at €1.22 billion, up 161 percent yoy. Of that figure, €478 million (+32.3 percent yoy) were recorded in 3Q21. As for risk indicators, the cost of risk declined to 0.32 percent ytd, compared to 0.8 percent a year earlier. The NPL and NPL coverage ratios improved during the quarter, standing at 4.1 and 66 percent, respectively, thanks to a drop in non-performing loans.

In Mexico, lending increased 3.4 percent compared to 2020 year-end, driven mainly by growth in retail segments. Customer deposits continued growing strong (+5.7 percent in 2021) on the back of demand deposits – with a positive impact in the financing mix – and mutual funds.

The net attributable profit stood at €1.81 billion in the first nine months of the year (+47.4 percent yoy), with NII growing 4.1 percent yoy, driven by an improvement in customer spreads, as well as fees and commissions (+15.5 percent) resulting from heightened activity and increased transactions. Regarding risk indicators, the cumulative cost of risk declined to 2.70 percent, above expectations, thanks to the solid portfolio performance. The NPL ratio improved to 2.5 percent and the NPL coverage ratio stood at 131 percent.

In Turkey, retail and commercial lending in local currency grew strongly (+29.7 percent), while foreign currency loans dropped (-11.1 percent). In the P&L account, NII saw a stronger recovery of 19.7 percent in 3Q21 vs. 2Q21, driven by activity in Turkish lira, improvement in spreads and a higher contribution of CPI-linked bonds. Thanks to this, the drop in cumulative NII yoy has shrunk to -4.9 percent (compared to a -10.1 percent yoy drop through June). Between January and September, net fees and commissions increased close to 45 percent yoy. The attributable profit through September stood at €583 million, 48.4 percent more than in the same period of 2020. The cumulative cost of risk declined to 0.88 percent, exceeding expectations, while the NPL and coverage ratios improved to 6.5 percent and 78 percent, respectively, thanks to high recoveries in the quarter.

In South America, lending increased 6.8 percent yoy, driven mainly by the retail portfolio. The net attributable profit stood at €339 million through September (+26.2 percent yoy), driven by recurring revenues (NII shows a 13.8 percent yoy growth, while net fees and commissions increased 34.9 percent). The cumulative cost of risk for the year stood at 1.87 percent, while the NPL and coverage ratios ended at 4.5 percent and 108 percent, respectively, at the end of September.

In the breakdown by country, it is worth mentioning the loan growth in Peru and Colombia (+5.7 percent and 4.1 percent yoy), both in retail and commercial segments. Despite the impact of hyperinflation, Argentina added €42 million to the Group’s earnings thanks to growth in fees and commissions and the contribution to NII from securities portfolios.

¹The non-recurring impacts include the results after tax from the sale of the U.S. business to PNC and the net costs related to the restructuring process of BBVA S.A. in Spain as of 09-30-21, as well as the goodwill charge of BBVA USA, recorded in 1Q20.

²These figures exclude the non-recurring impacts.

³This amount has been calculated as a 10 percent of the standing number of shares. (666,788,658) multiplied by share price as of July 22 (€5.251) reference date for the ECB request.

⁴The maximum number of shares to be acquired can not exceed 637,770,016 shares, representing approximately 9.6 percent of BBVA’s share capital at the time of the Board of Directors resolution.

⁵The pro forma CET1 ratio includes the deduction of the maximum amount of €3.5 billion of the share buyback program. Such deduction has been implemented in October as per ECB authorization.

About BBVA

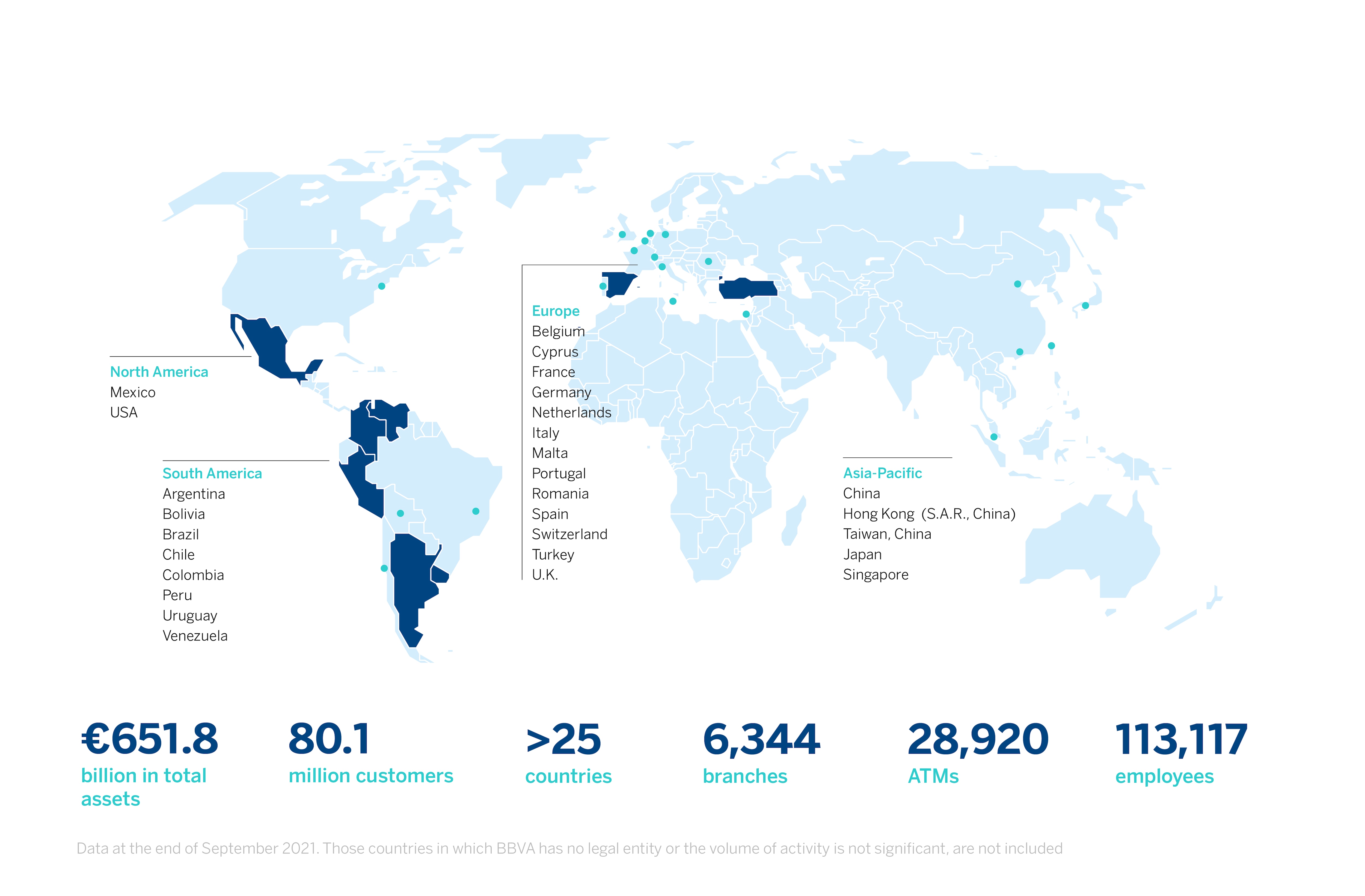

BBVA is a customer-centric global financial services group founded in 1857. The Group has a strong leadership position in the Spanish market, is the largest financial institution in Mexico and it has leading franchises in South America. It is also the leading shareholder in Turkey’s Garanti BBVA and has an important investment, transactional and capital markets banking business in the U.S. Its purpose is to bring the age of opportunities to everyone, based on our customers’ real needs: provide the best solutions, helping them make the best financial decisions, through an easy and convenient experience. The institution rests in solid values: Customer comes first, we think big and we are one team. Its responsible banking model aspires to achieve a more inclusive and sustainable society.