Corporate information

Letter from the Chair

Dear shareholders,

2025 was an outstanding year for BBVA. We significantly expanded our positive impact on all our stakeholders – clients, employees, shareholders and society as a whole –, and achieved the best results in our history.

During the year, 11.5 million new customers joined the Group – a new record –, 66 percent through digital channels. This growth reflects the strength of our value proposition and the strategic vision we launched more than a decade ago to lead the digital transformation of banking.

Thanks to this expanded reach, we supported more individuals and businesses at key moments in their lives and projects. In 2025, over 160,000 families gained access to a home; one million SMEs and self-employed individuals boosted their activity with new financing; and 73,000 large corporations made investments to grow and create jobs.

Furthermore, we channeled €134 billion into sustainable finance, supporting our clients in their transition toward a more sustainable economy. And we mobilized €30.2 billion for social initiatives, such as building hospitals, schools and infrastructure that are essential for development.

Together with the BBVA Foundation and the BBVA Microfinance Foundation, we allocated €192 million to social initiatives that benefited nearly eight million people.

None of this would be possible without the talent and commitment of the more than 127,000 people who make up BBVA. We are an innovative, ambitious and fully customer-oriented team that works every day to offer increasingly relevant and personalized solutions. Our ability to anticipate trends, incorporate new technologies and execute with discipline is the foundation of our impact and our results.

Value creation for shareholders

This impact and this execution capability are also reflected in the value created for you, our shareholders.

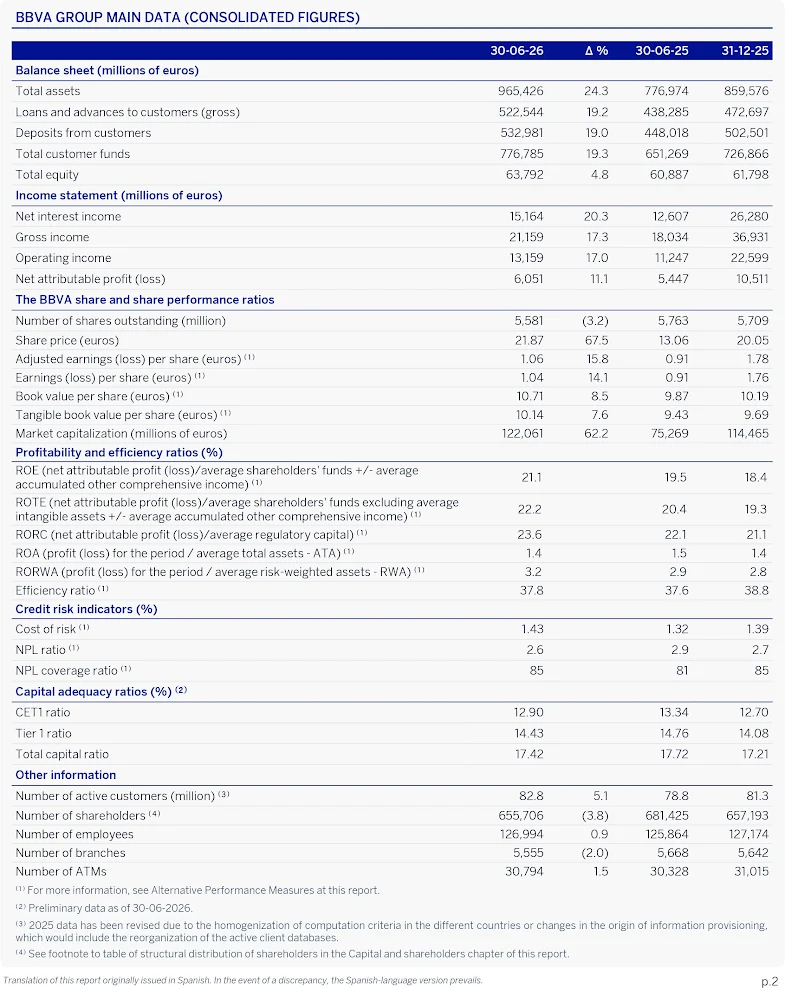

In 2025, we achieved a net attributable profit of €10.51 billion – 4.5 percent more than the previous year. We continued to be at the forefront of European banking both in growth and profitability: our loan portfolio increased by 16.2 percent in constant euros and return on tangible equity (ROTE) stood at 19.3 percent.

Tangible book value per share plus dividends rose by 12.8 percent during the year – by 15.2 percent excluding the impact of share buybacks – continuing the value creation trend of previous years.

We will distribute over €5.2 billion – half of our profit – against 2025 results. At the Annual General Meeting on March 20, we will propose a cash dividend of €0.60 per share. Together with the €0.32 per share paid in November, this would raise the total cash dividend per share to €0.92 – 31 percent more than the previous year and our highest dividend ever.

This is in addition to the €3.96 billion extraordinary share buyback program currently underway. In total, we will return over €9.2 billion to our shareholders, a reflection of our firm commitment to attractive, sustainable returns.

In addition, we currently hold a significant excess capital above the 12 percent level that will translate into greater distribution capacity in the future.

Looking at the bigger picture, since the start of 2019, the value of our shareholders’ investment – including dividends and share performance – has multiplied over six-fold, a return that is clearly superior to our main European and Spanish peers.¹

¹Value of the investment includes share performance plus dividends. European banks: Stoxx Europe 600 Banks. Spanish banks: BKT, CABK, SAB, SAN, UNI, weighted by market capitalization. Data from 01/01/2019 through 02/27/2026

Environment and artificial intelligence

The environment continues to be challenging, with trade tensions, international conflicts and rising fragmentation in the economic order. However, the global economy is showing greater resilience than expected. BBVA Research estimates point to 3.2 percent annual growth between 2025 and 2027, but the recent escalation of the conflict in Iran could weigh on growth momentum and lead to additional episodes of volatility.

But there is one aspect that stands out from previous cycles: artificial intelligence. It is not just a passing trend, but a structural transformation that is redefining how we create value, work and compete. It represents a challenge of enormous magnitude and at the same time, an extraordinary opportunity for those who know how to integrate it.

At BBVA we have decided to reinvent ourselves once again – just as we did with digitization – to lead the way once more.

Strategic Plan 2025-2029

Last year we launched our 2025-2029 Strategic Plan, with notable progress in our key priorities. A plan that revolves around a clear premise: incorporating a radical client perspective into everything we do. We want to better understand each customer, anticipate their needs and support them with increasingly relevant, personalized solutions.

With this goal in mind, the Plan reinforces our strategic priorities:

- Scale up all Enterprise segments

- Boost sustainability as a growth engine

- Promote value and capital creation

- Strengthen our empathy to succeed as a winning team

- Unlock the full potential of artificial intelligence

Artificial intelligence holds a central place in this new phase. We have laid out a roadmap with eight major initiatives, ranging from digital advisors for customers and bank agents to improvements in risk management, process automation and accelerated software development.

The strategic partnership with OpenAI expands our ability to scale these solutions, combining our global presence and customer knowledge with the most advanced technology. Building on our experience with digitization, this new technological transformation consolidates our leadership and reinforces our competitive advantage.

Financial ambition

The Strategic Plan includes ambitious financial targets that reflect our confidence in our ability to execute it. We aim to:

- Reach an average ROTE of around 22 percent in the 2025-2028 period

- Achieve efficiency levels close to 35 percent in 2028

- Generate annual growth of tangible book value per share plus dividends of around 15 percent for the 2025-2028 period

They are ambitious goals, fully aligned with a strict financial discipline and commitment to creating sustainable long-term value.

BBVA is at its best moment. We have leading franchises, a clear and unique strategy, a strong capital position and an exceptional team.

We will continue to work with ambition to lead the banking industry in the age of artificial intelligence, advance the sustainable transition and play a decisive role in the economic and social progress of all countries where we operate.

And to all of you, our shareholders, thank you for your trust and continued support.

Kind regards,

Carlos Torres Vila

Letter from the Chief Executive Officer

Dear shareholders,

2025 was a great year, with the best financial results in our history. We delivered a record net attributable profit of €10.51 billion, up 4.5 percent from the previous year. This performance consolidates our track record of sustained growth and once again demonstrates the strength of our diversified business model.

I would like to begin by thanking the more than 127,000 people who make up BBVA. These results are a direct reflection of their professionalism and commitment to our customers. In a demanding and changing environment, our teams once again showed remarkable adaptability and a clear focus on execution.

Business activity growth was particularly strong. Customer lending increased by 16.2 percent in constant euros, with market share gains in most of the countries where we operate. More importantly, this growth showed strong profitability. ROTE reached 19.3 percent, among the highest in European banking. This combination of growth, profitability, and efficiency strengthens our competitive position compared with our main European peers.

Financially, the year was defined by strong core revenues, which increased 14.1 percent in constant euros and drove gross income to €36.93 billion, up 16.3 percent from 2024. Excluding currency effects, net interest income grew 13.9 percent and net fees and commissions increased 14.6 percent, with broad-based growth across all business areas. This performance was supported not only by strong activity levels but also by disciplined pricing and balance sheet management.

At the same time, we maintained strict cost control. Revenue growth significantly outpaced expense growth, and we improved our efficiency ratio to 38.8 percent, placing us among the most efficient banks in Europe. Operating income reached an all-time high of €22.60 billion, up 20.4 percent in constant euros from the previous year.

Risk indicators performed favorably and in line with our expectations. The cumulative cost of risk stood at 1.39 percent, the NPL ratio improved to 2.7 percent, and the coverage ratio rose to 85 percent. All of this occurred against a backdrop of strong credit growth, reflecting the quality of our origination and prudent risk management.

Our capital position remains solid. The CET1 ratio reached 12.70 percent at year-end, even after accounting for the dividend and the €3.96 billion extraordinary share buyback program we are executing. We remain committed to distributing any excess capital above the upper end of our CET1 target range (12 percent). This strong capital base allows us to continue growing strongly and deliver attractive shareholder returns.

By business area, Spain and Mexico once again demonstrated their structural strength.

In Spain, lending grew 8 percent year over year, with particularly strong performance in corporate and consumer segments. Net attributable profit reached its highest level ever, €4.18 billion, up 11.3 percent from 2024, driven by core revenue growth, disciplined cost control, and lower impairment charges. Risk indicators continued to improve, with a cost of risk of 0.34 percent.

In Mexico, the loan portfolio grew 7.6 percent, with strong growth in retail segments. Net attributable profit reached €5.26 billion, up 5.7 percent at constant exchange rates. Also noteworthy are the strong risk indicators along with the efficiency, which remained strong at around 30 percent, a clear differentiator within the local financial system.

Turkey delivered net attributable profit of €805 million, up 31.8 percent in current euros, driven by core revenue growth and a lower impact from hyperinflation adjustments. The performance of risk indicators points to a normalization process following an extended period of negative real interest rates.

In South America, lending grew 13.9 percent year over year, and net attributable profit reached €726 million, with particularly strong performance in Peru and Colombia. Risk indicators evolved favorably and in line with our expectations.

In the Rest of Business area—which primarily includes wholesale banking (CIB) in Europe (excluding Spain), the United States and Asia, as well as our digital banks in Italy and Germany—net attributable profit totaled €627 million, up 29.4 percent year over year at constant exchange rates. Growth was driven by project finance, corporate lending, and primary market issuances.

Overall, the performance of our franchises confirms the strength and diversification of our business model, as well as our execution capabilities in very different environments.

2025 marked the first year of our new Strategic Plan, and we are advancing at a steady pace. We added 11.5 million new customers and grew in particularly relevant strategic segments, such as enterprises and sustainable business. Putting customers at the center is the foundation of this plan. It has enabled us to become one of the most recommended banks in all our markets.

Applying artificial intelligence is vital to the evolution of our management and the development of our business. These tools are already leading to tangible improvements in productivity and operational quality and helping to strengthen our risk management standards.

Our objective is clear: apply technology where it creates measurable impact in efficiency, customer experience and risk control. This combination is what underpins a lasting competitive advantage.

As we enter 2026, we expect to sustain positive momentum, delivering growth above our peers and profitability of around 20 percent. We start from a position of strength: leading franchises, profitability and efficiency levels that set us apart from our European peers, and a solid capital base.

We will continue to execute our strategy with a clear focus on profitable growth, prudent risk management, and sustainable value creation for all our shareholders.

Kind regards,

Onur Genç

Chief Executive Officer

History of BBVA

The history of BBVA is the history of many different people; people who have been a part of the more than one hundred financial institutions that have joined our corporate journey since it first began in the mid-19th century. Today, at BBVA we work to support our clients their drive to go further..

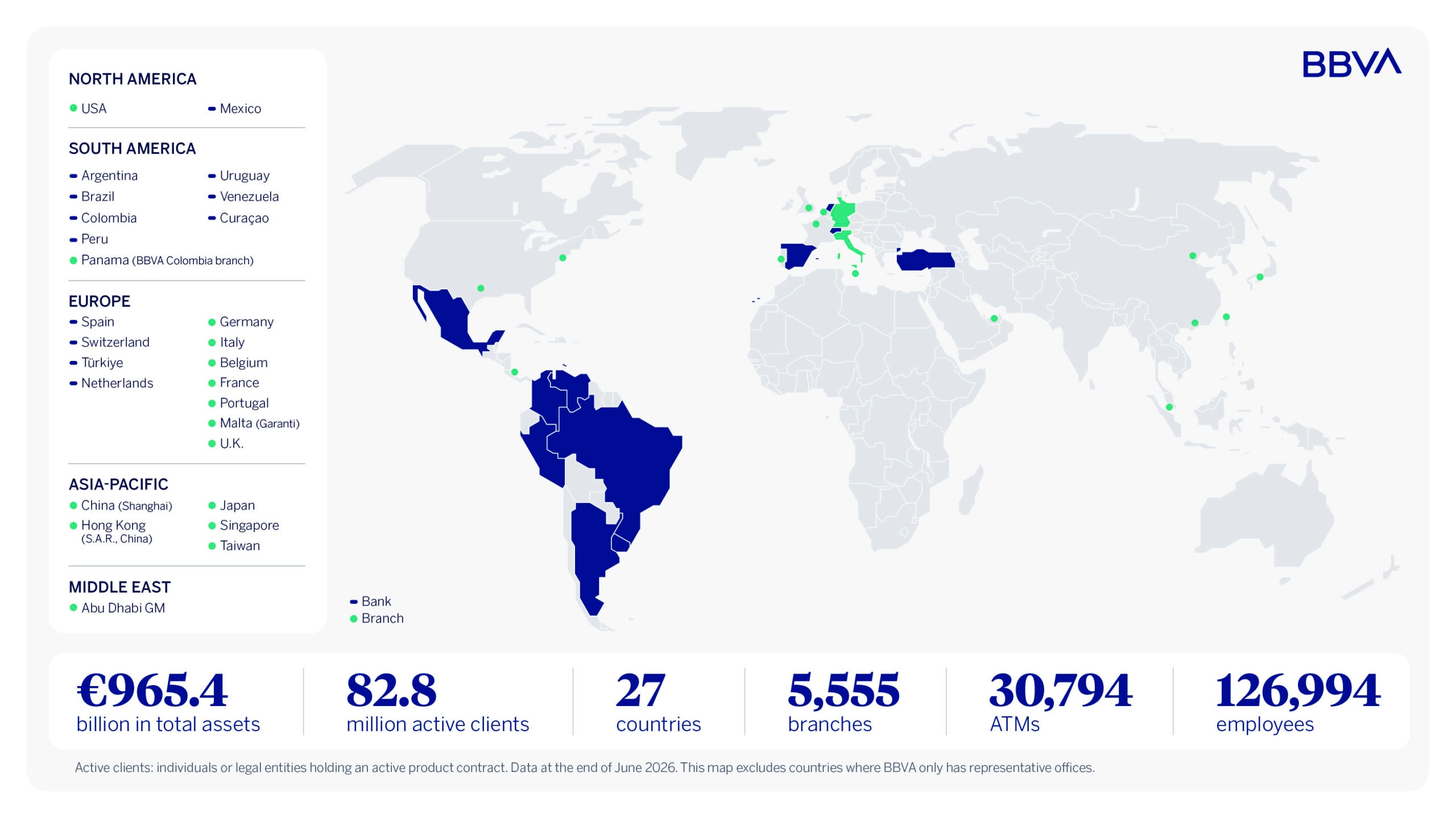

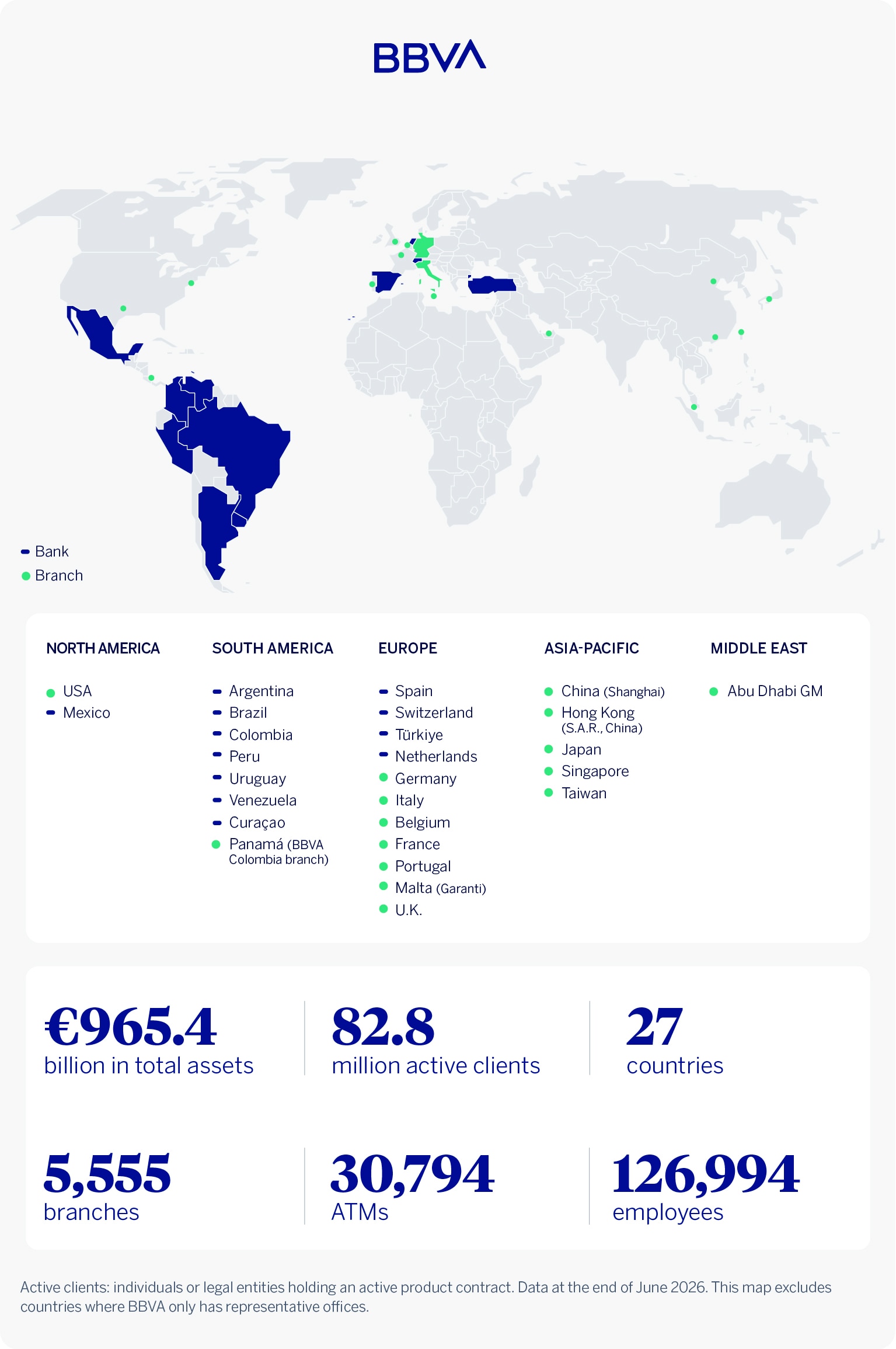

BBVA in the world

BBVA is a global financial group with a customer-centric vision, characterized by its pioneering strategy in digitalization, innovation and sustainability. BBVA holds a leading position in Spain, is the largest financial institution in Mexico, and has leading franchises in South America and Turkey. In Europe, BBVA has a steadily growing presence, driven by its specialized offices serving business customers and its focus on digital banks, currently operating in Italy and Germany. In addition, BBVA provides specialized services to large corporations through its offices in the United States and Asia. This strong geographic diversification, together with high levels of customer acquisition through digital channels, positions us to strengthen our leadership and address the challenges of the future.

BBVA contributes with its activity to the progress and welfare of all its stakeholders: shareholders, clients, employees, providers and society in general. In this regard, BBVA supports families, entrepreneurs and companies in their plans, and helps them to take advantage of the opportunities provided by innovation and technology. Likewise, BBVA offers its customers a unique value proposition, leveraged on technology and data, helping them improve their financial health with personalized information on financial decision-making.

Basic data

Relevant data of the BBVA Group (consolidated figures) at 30-06-2026. This section contains all the updated quarterly figures on the balance sheet and income statement, and other relevant data.

More financial information is available on the Shareholders and Investors website.

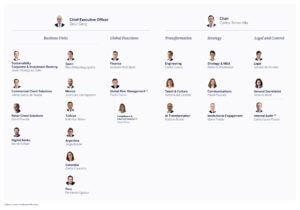

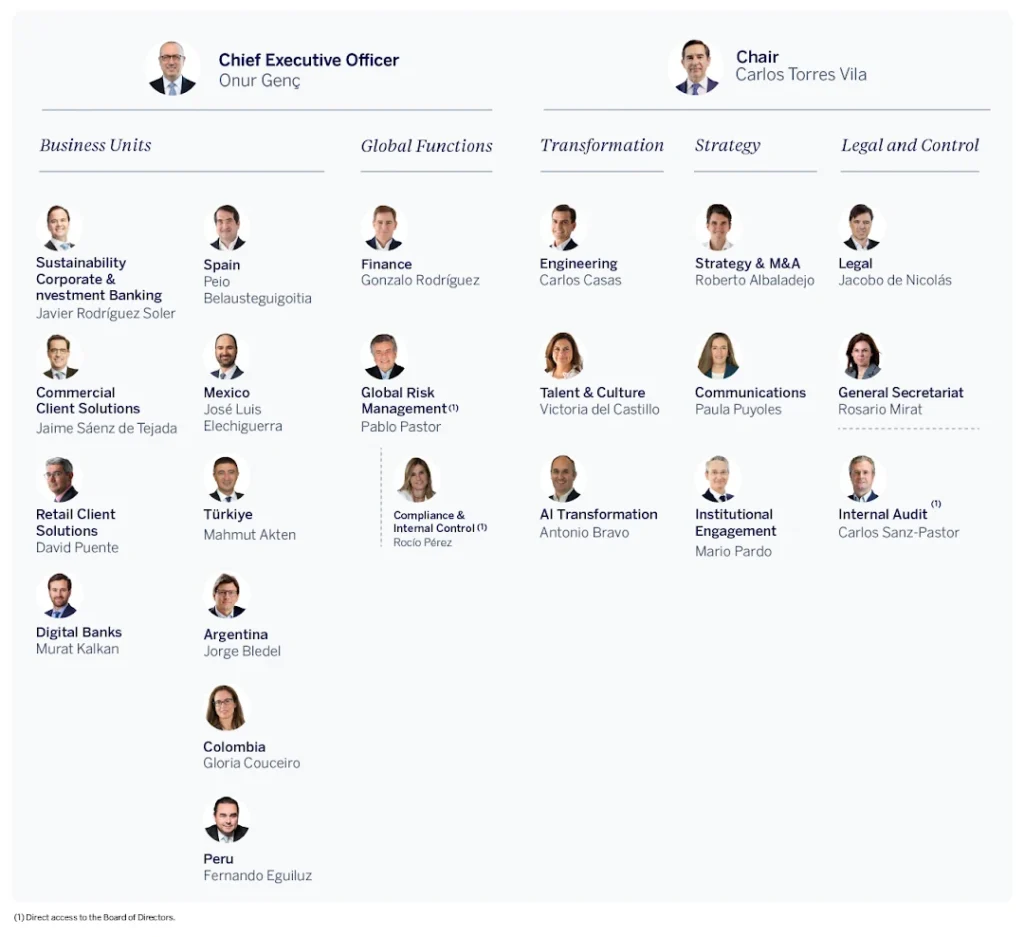

Organizational chart

Organizational structure

BBVA’s organizational structure meets the objective of continuing to promote the transformation and businesses of the Group, while advancing in the delimitation of executive functions.

The Chair is responsible for the management and proper functioning of the Board of Directors, the supervision of the Group’s management, institutional representation, and leading the Group’s strategy and transformation process. Meanwhile the Chief Executive Officer (CEO) is in charge of the daily management of the Group’s businesses, reporting directly to BBVA’s Board of Directors.

Additionally, certain control areas (Internal Audit and Regulation & Internal Control) report directly to the Board of Directors through its corresponding committees.

Strategy

The current macroeconomic environment is marked by geopolitical tensions, a normalisation of interest rates and an increasing ageing of the population, which will generate challenges and opportunities in the financial sector.

In addition, the rest of the long-term global trends on which BBVA's strategy is based and which play a critical role in the transformation of the economy have continued to consolidate and evolve.

- Digitization has continued to solidify across most sectors, ushering in a new era of disruption driven by artificial intelligence (AI). AI is redefining competitive dynamics across numerous industries, including the financial sector, and its impact on the entire value chain is creating significant opportunities:

-

- Hyper-personalization of value propositions.

- Process automation, expected to have a profound effect on middle and back-office tasks, improving data control, productivity, and customer experience.

- The continued advancement of technologies such as blockchain, quantum computing, and cloud processing, which are opening up a transformative era of opportunities for society and the financial industry.

At the same time, the financial system is navigating an increasingly complex competitive landscape, with the rise of new digital competitors, such as neobanks, and non-bank players disrupting traditional models.

- Sustainability will remain a key driver of economic growth:

-

- Investments in the transition to a decarbonized economy are gaining momentum, fueled by increasing energy demand and the cost-effectiveness of renewable energy sources. Additionally, profitability in emerging technologies is rising, thanks to ongoing innovation. It is currently estimated that approximately half of the emissions reductions required will come from technologies that are still in their early stages and unproven on a large scale.

- Banks will play a crucial role in this transition by channeling investments and providing guidance to their clients as they move toward a decarbonized and more energy-efficient economy in the context of growing energy demand.

- Moreover, investments aimed at enhancing production processes and improving the value chains of companies that contribute to preserving natural capital are also on the rise. Reversing the depletion of natural capital is essential due to the significant economic and financial impacts it entails.

Purpose and values

BBVA’s strategy revolves around a single Purpose: “Support your drive to go further”.

- Support means being consistently present, especially during life’s most critical moments. It involves providing ongoing assistance to customers, actively listening to them, understanding their needs, and adapting accordingly. At the heart of this is empathy: it allows BBVA to connect deeply with its customers, aligning with their concerns, aspirations, and dreams, and becoming a trusted ally that genuinely understands what its customers need.

- Your drive. BBVA understands that behind every project, every goal, and every step forward lies something deeper: a drive. It’s that inner strength that inspires people to excel, pursue their ambitions, and believe in a brighter future. It’s the determination to keep moving forward, the motivation fueling them every day.

- To go further embodies the spirit of progress and innovation. It reflects an attitude that is deeply ingrained in BBVA’s DNA, always striving to anticipate, to envision today what the future holds, and to approach tomorrow with optimism. This ability to foresee and adapt creates immense value for the individuals and businesses that choose BBVA as their trusted partner to achieve their dreams.

The customer comes first

BBVA places customers at the center of its activity, before anything else. The Bank aspires to take a holistic customer vision, not just financial. This means working in a way which is empathetic, agile and with integrity, among other things.

- We make our customers’ needs our own: we take on our customers’ needs as our own, responding swiftly and effectively. We anticipate challenges and provide continuous support.

- We are empathetic: we put ourselves in others’ shoes, listen attentively, tailor our response to their needs, and act with respect to ensure everyone feels valued.

- We have integrity: we always act with honesty, in compliance with the law and BBVA’s internal regulations, without tolerating inappropriate behavior. We are a trusted partner, providing support with transparency and responsibility.

We think big

It is not about innovating for its own sake but instead to have a significant impact on the lives of people, enhancing their opportunities. BBVA Group is ambitious, constantly seeking to improve, not settling for doing things reasonably well, but instead seeking excellence as standard.

- We are ambitious: we drive a positive impact on people’s lives and society as a whole. We support their desire for growth and progress.

- We are innovators: we stay ahead of challenges by offering agile and effective solutions. We create value-driven proposals to help our customers go further.

- We exceed customer’s expectations: we create effective solutions that exceed customer expectations. We help individuals and businesses reach their full potential.

We are one team

People are what matters most to the Group. All employees are owners and share responsibility in this endeavor. We tear down silos and trust in others as we do ourselves. We are BBVA.

- I am committed: I take on the bank’s objectives as my own, feeling a genuine connection with BBVA’s values and purpose, which drives me to work with passion and enthusiasm.

- I trust others: we collaborate with generosity and trust, ensuring clear and respectful communication. Together, we drive the growth of our customers and our team.

- I am BBVA: we are a global and diverse team that shares a common purpose and creates a positive impact. We support, inspire, and drive people and businesses to reach further.

Strategic priorities

BBVA has defined six strategic priorities, focusing on:

- Differentiation.

- Full commitment to growth and value creation.

- Meaningful impact across the board.

1 - Embed a Radical Client Perspective in all we do

- It is the core of our strategy and impacts everything we do.

- The goal is to offer a value proposition focused on the needs of our clients and their financial health, ensuring a coherent, fluid and quality experience across all their channels.

- A new way of interacting with our clients with a focus on hyper-personalization and real-time contextualization, taking advantage of new technologies such as artificial intelligence.

- Achieving excellence in execution, always being available and ensuring that 100% of interactions are positive.

2 - Boost sustainability as a growth engine

- BBVA was a pioneer in identifying the impact of sustainability on competitive dynamics in all industries, including both the environmental and social axis.

- Sustainability must become a driver of differential growth in the banking business, taking advantage of the need to finance investments to meet a growing demand for efficient and clean energy.

- Specialized advice tailored to each market segment and the transformation of risk processes are key to generating differential growth.

3 - Scale up all enterprise segments

- BBVA wants to be the benchmark bank for the business segment (SMEs, companies, institutions and large corporations, which will be a key driver of differential growth.

- We have great competitive advantages, such as our presence in 25 countries, which allows us to better meet the needs of global companies, and also our specialization in sustainability.

- A stronger corporate business that complements the retail business, offering a comprehensive universal banking proposal compared to new competitors with a presence only in the retail segment.

- BBVA wants to promote this priority, taking advantage of the radical focus on the customer, with specialized advice and through the continuous improvement of its digital capabilities and technological platforms, with a focus on optimizing risk processes to speed up response times.

4 - Promote a value and capital creation mindset

- We want to continue to advance in the concept of profitable growth, closely linked to our strategy and the generation of long-term value.

- All processes must consider value creation as a critical factor for decision-making. This implies changes in management models, incentives, monitoring and reporting. Initiatives such as balance sheet rotation are key to optimizing the use of capital and maximizing profitability, while allowing for a greater positive impact on the client.

- This priority reinforces the importance of low-capital consumption and high-value creation businesses such as: insurance, private banking, asset management and payment ecosystem.

5 - Unlock the potential of AI and innovation through data availability and Next Gen Tech

- Responsible use of data and new technologies has always been a key factor in BBVA's strategy.

- The availability of data is a critical step in being able to generate a differential impact throughout the value chain, both on customers, through a hyper-personalized proposal and added value, and on efficiency and control thanks to process automation.

- The evolution to new generation technologies (Next Gen) is essential to efficiently address all the requirements derived from hyper-personalization and increased interactions with customers.

6 - Strengthen our empathy, succeed as a winning team

- All of us who are part of the BBVA team are a fundamental factor in the execution of the strategy.

- We are a team that is proud to be part of BBVA, that connects with the purpose and values, that does not settle and always seeks excellence and a differential added value for the customer. For this reason, it is necessary to foster empathy throughout the organization to radically adopting the customer perspective.

- The new priorities require a team with a winning and ambitious character to continue leading the transformation.

Sustainable and responsible business model

BBVA is committed to helping its customers move toward a more sustainable future. Sustainability is one of the bank’s six strategic priorities and is central to its business. This commitment spans several dimensions across the countries where BBVA operates.

-Climate. Projects related to global warming: electric transportation, energy efficiency, renewable energy, etc.

-Natural capital. Projects related to nature: water, land, biodiversity, and waste and pollution.

-Inclusive growth. Projects related to inclusive social and economic growth: inclusive infrastructure, financial inclusion, entrepreneurship, job creation, access to basic goods and services.

BBVA aims to promote sustainability as a driver of growth and, through it, to foster new business. The bank has set itself a new sustainable business channeling target of €700 billion from 2025 to 2029. This means more than doubling the previous target, which was to channel €300 billion between 2018 and 2025. The bank achieved this goal in December 2024, a year ahead of schedule. The new, more ambitious target is also set for a shorter period (five years instead of eight).

BBVA continues with its Transition Plan to achieve Net Zero by 2050. The bank has set decarbonization targets for 2030 in ten sectors:oil and gas, electricity, automotive, steel, cement, coal, aviation, maritime transport, aluminum, commercial and residential real estate.

Moreover, BBVA is committed to making a positive impact on society with a focus on education and support for entrepreneurship. BBVA allocated €191.5 million to social programs and initiatives in 2025 globally, an increase of 7.5 percent over 2024. 7.7 million people directly benefited from these activities, which mainly focused on education, accounting for 68 percent of the total resources. These efforts aimed to facilitate access to opportunities and support people and communities in their development.

Sustainability is fully integrated into the organization with a solid governance model. In 2021, BBVA elevated sustainability to the highest executive level of the organization, reporting directly to the CEO and Chair, and created the global Sustainability business area headed by Javier Rodríguez Soler. The area designs the strategic sustainability agenda, specifies and promotes the lines of work in this area in the various global and transformation units, and develops new sustainable products, in a context in which all employees and areas of the Group integrate sustainability into their day-to-day work.

The bank also has a network of experts, made up of sustainability specialists, who are responsible for generating knowledge in this field to accompany clients, support the areas in the development of new value propositions in this area, integrate climate risks into risk management and define a public agenda and sustainability standards.

BBVA’s Code of Conduct

The Code of Conduct establishes the behavioral guidelines that, according to the principles of the BBVA Group, ensure that conduct adheres to the internal values of the Organization. To this end, it establishes the duty to respect applicable laws and regulations for all its members in an integral and transparent manner, with the diligence and professionalism that correspond to the social impact of financial activity and to the trust that shareholders and customers have placed in BBVA.

The Code was approved by the BBVA Board of Directors on July, 2026.

BBVA's Whistleblower Channel

A fundamental mechanism to guarantee the effective application of the regulations and guidelines of the Code of Conduct is the Whistleblower Channel, through which not only BBVA employees, but also other third parties not belonging to the BBVA Group can can confidentially and, if they wish, anonymously report any conduct that does not adhere to the Code of Conduct or that violates applicable legislation, including human rights-related complaints.

The Compliance area will handle complaints diligently and promptly. The information will be analyzed objectively and impartially and the identity of the whistleblower will be kept confidential. Those who report facts or actions in good faith through the Whistleblower Channel will not be subject to retaliation or suffer adverse consequences for this communication.

This Channel allows you to maintain, if you wish, a dialogue with the Manager of your complaint. For this purpose, we have designed a system (secure mailbox) that will allow you to communicate with BBVA, preserving your anonymity at all times.

The Whistleblower Channel is available 24 hours a day, 365 days a year from any computer or cell phone.

If you observe or someone informs you of an action or situation related to BBVA that may be contrary to the regulations or the values and guidelines of our BBVA Code of Conduct, please report it through:

Submit report on Whistleblowing Channel

The Whistleblower Channel is not the appropriate channel for dealing with customer complaints.

BBVA’s tax strategy

BBVA’s corporate principles for tax issues and fiscal strategy, approved by the Board of Directors.

BBVA Due Diligence

Know more about our regulatory framework, financials reports, Corporate Governance and Corporate Integrity Models.